Perception:

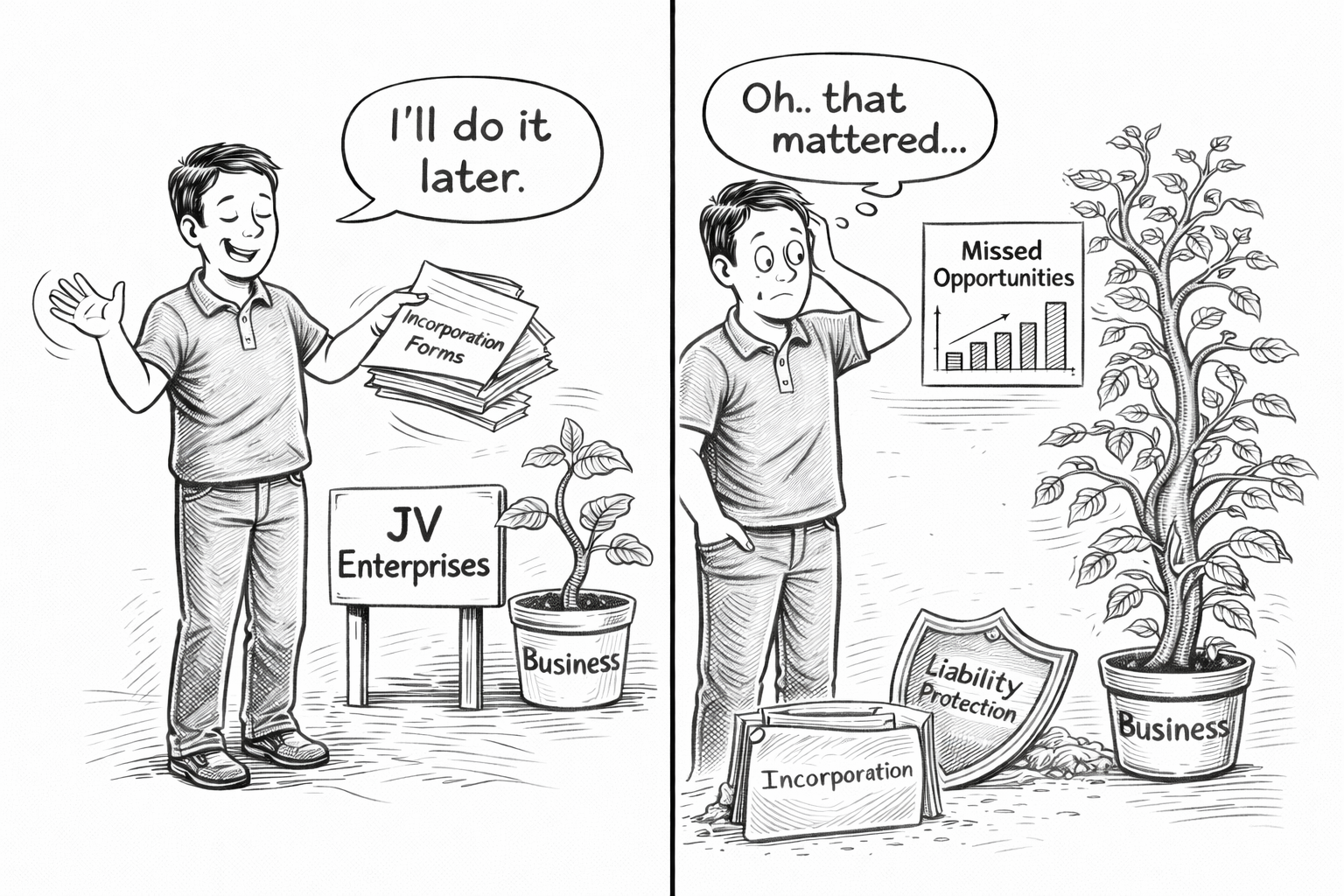

I’m not big enough yet. Incorporation can wait.

Reality:

Business structure determines flexibility, liability separation, and future tax options. Restructuring later is often more costly than structuring properly at the start.

Javier had been running his business as a sole proprietor for three years.

Revenue was growing. Clients were steady. Cash flow was improving.

Friends had mentioned incorporating.

His accountant had casually suggested it.

But Javier always gave the same answer.

“I’m not big enough yet.”

To him, incorporation felt like something you did when you had a large team, a formal office, and a six-figure salary.

He saw it as a milestone.

Not a foundation.

So he waited.

And while he waited, several things quietly happened.

All business income flowed directly into his personal tax return.

As revenue increased, so did his marginal tax rate.

There was no ability to retain earnings inside the company structure.

There was no separation between personal and business liability.

There was no flexibility in how compensation could be structured.

And there was no long-term planning around distributions, retirement strategy, or risk insulation.

But because nothing had gone wrong, Javier assumed nothing was wrong.

That assumption is common.

Many business owners treat incorporation as a badge of success rather than a strategic decision.

But structure shapes options.

A sole proprietorship is simple.

It is also limited.

An incorporated entity creates additional compliance responsibilities. It requires bookkeeping discipline. It introduces corporate filings and administrative costs.

But it also creates:

Potential tax deferral opportunities.

Liability separation between business and personal assets.

More flexibility in compensation planning.

Clearer operational structure.

Incorporation is not always necessary immediately.

But postponing it without evaluation is not strategy.

It is avoidance.

When Javier finally incorporated, he realized something uncomfortable.

Had he structured earlier, he could have retained earnings during higher-income years, smoothed personal tax exposure, and separated certain risks.

Instead, restructuring required adjustments, legal filings, and transitional complexity.

Waiting had not been free.

It had been expensive in ways he did not see at the time.

The calm business owner does not incorporate emotionally.

He evaluates timing strategically.

He asks:

What are my growth projections?

What is my liability exposure?

What tax bracket trajectory am I on?

What flexibility might I need in three to five years?

Structure is not about ego.

It is about options.

When business owners treat incorporation as something to “do later,” they often delay decisions that affect every myth that follows.

And delayed structure leads directly into the next misunderstanding.