About the Book, the Author and Important Notice

Return to Table of ContentsWhy This Book Matters

Every business owner has heard them.

“You can write that off.”

“If you didn’t make a profit, you don’t owe anything.”

“Just move it into next year.”

“My accountant will handle it.”

And the big one:

“If you ever get a letter from the IRS, you’re screwed.”

These statements are repeated with confidence.

That is what makes them dangerous.

Most tax problems are not caused by dishonesty.

They are caused by certainty built on incomplete understanding.

Assumptions passed from one owner to another.

Advice given casually.

Beliefs that feel reasonable.

Over time, those beliefs become habits.

Habits shape records.

Records shape filings.

Filings shape consequences.

The cost is rarely immediate.

It accumulates quietly in penalties, missed deductions, unnecessary risk, strained conversations, and sleepless nights.

This book was written to confront those assumptions directly.

Not emotionally or dramatically but clearly.

And with clarity comes wisdom.

Each chapter isolates a commonly accepted tax belief and examines it under pressure:

The Myth.

The Perception.

The Reality.

Some myths are partially true.

Some are outdated.

Some are simply wrong.

All of them deserve scrutiny.

Because in business, what you are confident about can either protect you or expose you.

This book is not about fear.

It is about discipline.

And discipline removes doubt before doubt has a chance to grow.

About the Author

Paul Neill is an entrepreneur, teacher, and author with over 45 years of experience building and operating small businesses across multiple industries.

Over the course of his career, he has worked alongside business owners who are skilled in their craft yet often uncertain about the financial and tax consequences of everyday decisions.

Paul is known for explaining complex subjects in clear, direct language. His work emphasizes disciplined systems that reduce risk, eliminate unnecessary stress, and support strong, defensible records.

As Founder of Tax Ready Ledger Co., he helps business owners maintain clean, consistent books that support confident tax filings and sound business judgment.

Tax Myths Exploded reflects his conviction that most tax anxiety is not caused by complexity. It is caused by assumptions left unexamined.

Replace assumption with clarity, and confidence follows.

Important Notice

The purpose of this book is knowledge.

And knowledge, applied carefully, guides important decisions.

It is designed to clarify common tax assumptions and improve the way business owners think about record-keeping and financial responsibility.

The examples used throughout reflect real-world business situations, including experiences drawn from the author’s own professional history. Names and identifying details have been modified where appropriate for clarity and privacy.

Myth #1

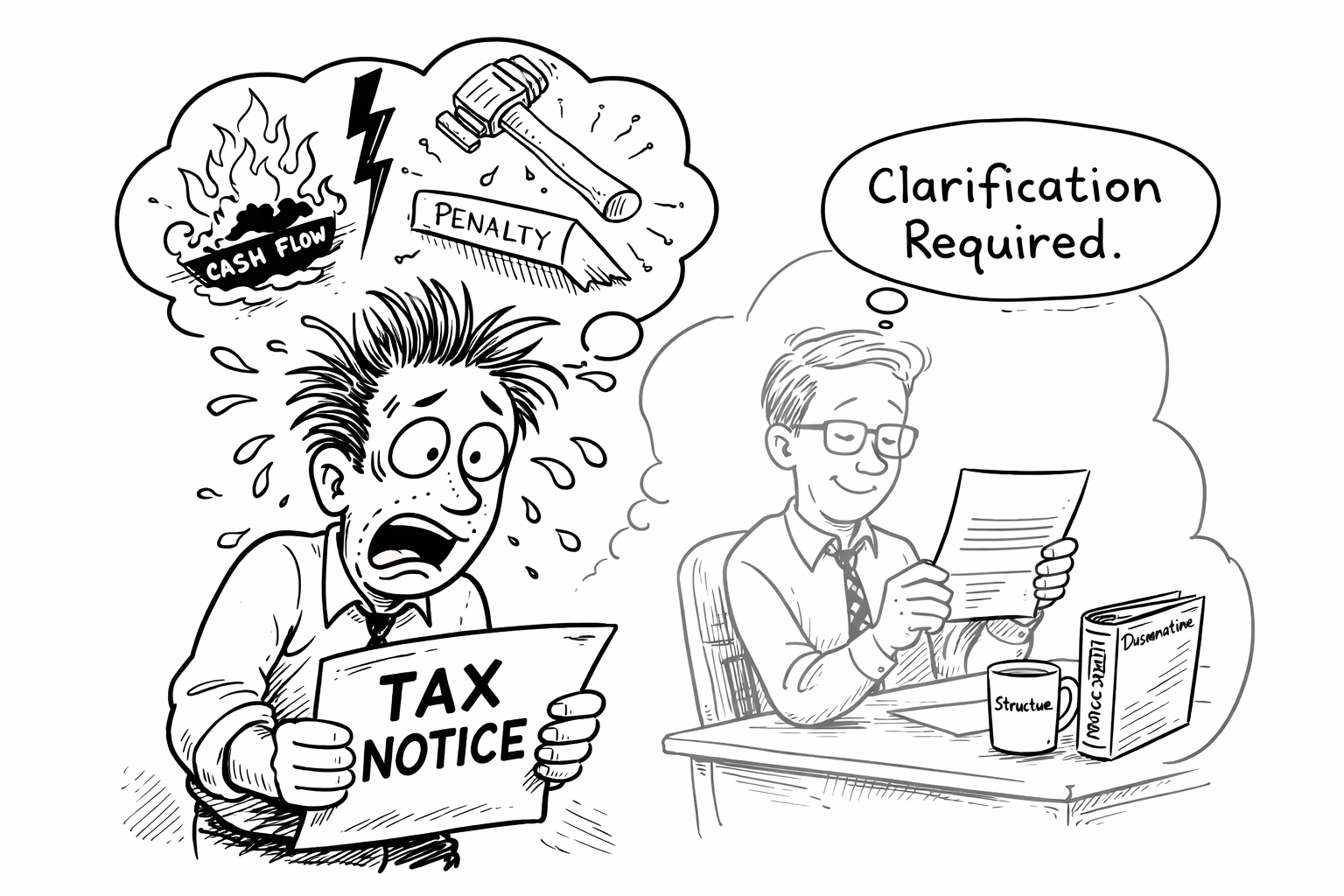

A Letter From the Tax Authority Means I’m in Serious Trouble

Perception:

If I receive a notice reassessing my return, something has gone terribly wrong.

Reality:

Tax authorities issue notices based on available data. Calm, documented responses often resolve misunderstandings without escalation.

Twelve years ago, as I was going through the day’s mail, one letter glaringly stood out.

It was from the IRS.

Those three letters carry weight…even fear. Most business owners do not open them casually.

And this was not one of the routine notices the IRS sends out.

I quickly scanned the letter.

Then I saw the assessment.

An additional $50,000 in taxes owed.

Fifty thousand dollars!

An extra $50,000 would have severely hurt my cash flow. It would have disrupted operations. It would have forced difficult decisions.

For a brief moment, fear spoke loudly.

Had I missed something?

Was this the beginning of something far worse?

Was I about to enter a battle I was not prepared for?

I put the letter down.

Then I picked it up again and read it slowly, carefully, line by line.

On that second reading, the emotion faded.

And I knew exactly how I needed to respond.

At the time, I was running a music education business that operated very differently from a traditional brick-and-mortar school. I traveled from city to city across the United States, renting hotel meeting rooms and conducting live workshops.

Participants experienced my method firsthand. Those who believed in it enrolled immediately.

Ninety-nine percent of my sales were processed by credit card in those hotel meeting rooms.

The IRS letter explained that based on comparable schools, the average volume of credit card sales in similar businesses was approximately 60 percent. Because I reported nearly all of my revenue through credit cards, they concluded I must be underreporting income.

In other words, my numbers did not match their averages.

But averages do not define reality.

Structure does.

Instead of reacting emotionally, I responded structurally.

I explained the nature of my business model. I documented that I rented hotel meeting rooms across multiple cities and conducted enrollment-based workshops. I provided supporting documentation reflecting how sales were generated and how the business operated. My travel expenses aligned with the structure and scope of that model.

I did not argue.

I clarified.

A few weeks later, another letter arrived.

The IRS accepted my explanation.

No further action was necessary.

The matter was closed.

An IRS notice is not a verdict.

It is a request for clarification based on available data.

Tax systems compare patterns. When numbers fall outside statistical norms, a notice is generated.

Fear interprets the notice as punishment.

Structure recognizes it as procedure.

The calm business owner understands the difference.

Documentation replaces anxiety.

Clarity replaces panic.

Preparation replaces sleepless nights.

Most business owners never move past the fear stage.

And that fear fuels the next myth.

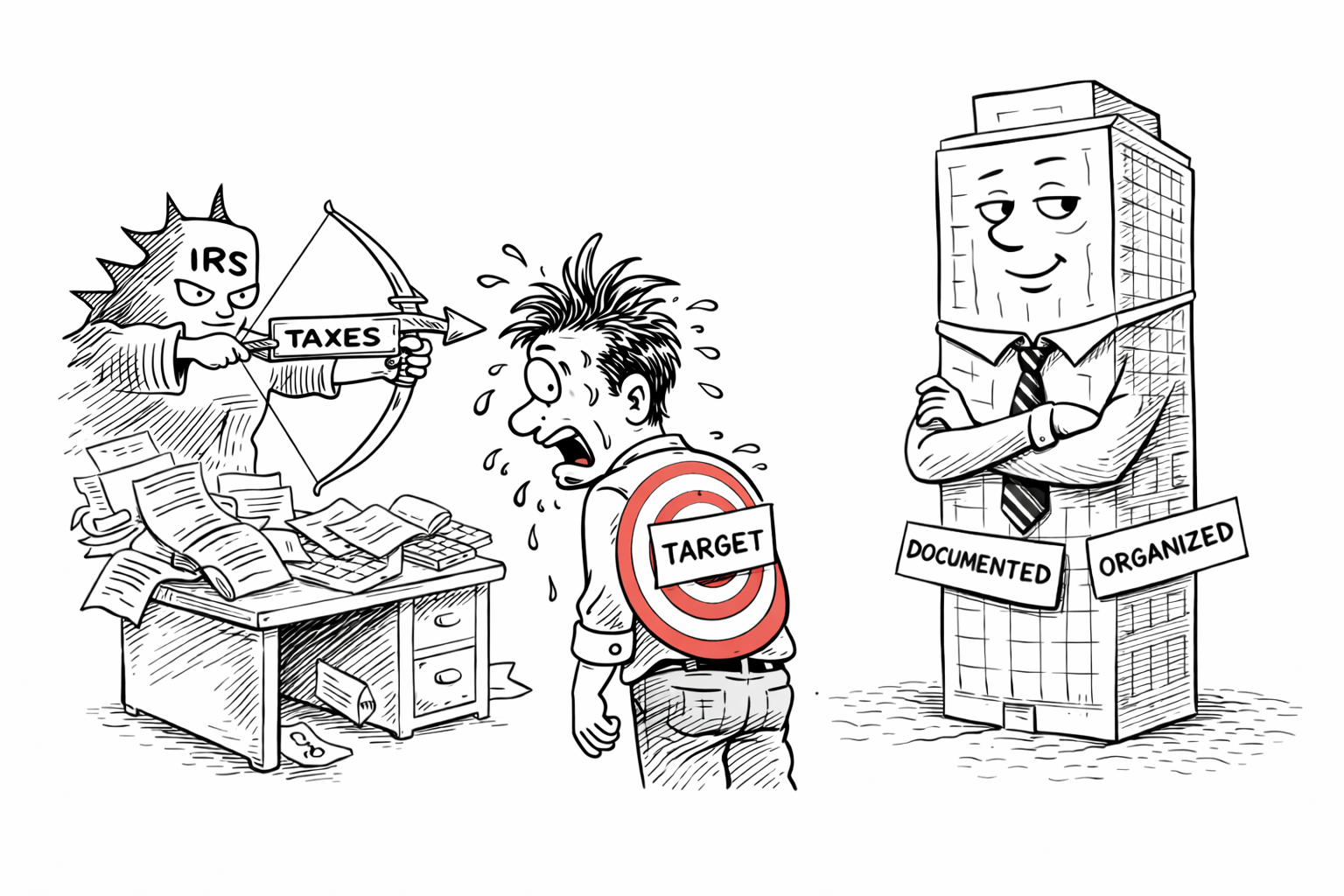

Myth #2

The Tax System Is Out to Get Me

Perception:

The rules favor the big players. Small business owners don’t stand a chance.

Reality:

The rules are impartial. They reward structure and penalize disorder because ignorance of the law excuses no one.

After receiving that IRS letter years ago, I understood something important.

The real problem was not the notice.

It was the narrative.

Many business owners carry a quiet belief in the back of their minds:

The system is rigged.

The IRS targets small businesses.

Big corporations get loopholes.

The little guy gets squeezed.

It is an easy story to believe.

Taxes are complex. The language is technical. The enforcement agency feels distant and powerful.

And when something goes wrong, it feels personal.

But here is the uncomfortable truth.

The tax system is not emotional.

It does not wake up angry.

It does not decide to pursue one business owner because it dislikes them.

It runs on rules.

Those rules are often dense, sometimes frustrating, occasionally inefficient.

But they are not personal.

They are structural.

When a business owner says, “The system is out to get me,” what they often mean is:

“I do not fully understand how this system works.”

And misunderstanding breeds fear.

Fear breeds resentment.

Resentment prevents learning.

Daniel learned this the hard way.

His bookkeeping was inconsistent. Some months were neat. Others were scattered across receipts, email confirmations, and half-updated spreadsheets.

He waited until the last minute to file.

Every year.

He rarely reviewed financial reports during the year. He only looked at numbers when tax season forced him to.

And every April, he felt the same frustration.

“I always pay too much.”

Instead of asking why, he assumed unfairness.

He blamed the system.

He blamed his accountant.

He blamed tax rates.

He blamed “loopholes” other businesses must be using.

What he did not examine was his own disorder.

Large corporations appear to “win” not because the rules love them.

They win because they build structure around the rules.

They hire teams.

They document aggressively.

They plan years in advance.

They operate within frameworks.

The rules reward preparation.

They penalize disorder.

That is not favoritism.

That is predictability.

When Daniel began keeping clean monthly books, reviewing financial statements regularly, and making decisions before year-end instead of after it, something surprising happened.

The resentment faded.

Not because tax rates changed.

Because clarity replaced chaos.

When you understand how tax authorities interpret data, how compliance thresholds work, how classification rules are defined, and how documentation supports your position, the system becomes far less intimidating.

It becomes mechanical.

And mechanical systems can be learned.

The calm business owner does not assume hostility.

He assumes responsibility.

He does not blame the system.

He studies it.

He does not complain about complexity.

He builds structure around it.

The tax system is not out to get you.

But it will expose disorder.

And disorder, when examined honestly, always reveals opportunity for structure.

Most business owners never move past resentment.

And that resentment fuels the next myth.

Myth #3

My Accountant Will Handle It

Perception:

I don’t want to worry about tax matters. That’s why I hire a professional.

Reality:

Accountants interpret the numbers they receive. But ultimate responsibility remains with the business owner.

After gaining control of her day-to-day bookkeeping, Elena felt a sense of relief.

She hired a reputable accountant.

Problem solved.

Or so she believed.

Many business owners assume that hiring an accountant transfers responsibility.

It does not.

It transfers interpretation.

An accountant works with the information provided.

If revenue is incomplete, the return reflects incomplete revenue.

If expenses are misclassified, the return reflects those classifications.

If documentation is thin, deductions may be limited.

An accountant is not a mind reader.

He is an interpreter.

Elena gathered her documents once a year and forwarded them without much review. She rarely looked at her profit and loss statements. She did not ask planning questions before year-end. She assumed the accountant would “optimize everything.”

One year, she failed to properly separate personal and business vehicle expenses. She assumed the accountant would sort it out. Instead, conservative adjustments were made because the documentation was unclear. She paid more than necessary, not because the accountant was careless, but because the information was incomplete.

Compliance happened.

Strategy did not.

This distinction matters.

Filing a tax return correctly is compliance.

Structuring a business efficiently is strategy.

Most accountants focus primarily on compliance. They report what happened.

They cannot redesign what should have happened if they are brought in after the fact.

Delegation does not eliminate accountability.

History offers public reminders of this principle.

Willie Nelson faced significant IRS action in the 1990s that resulted in the seizure of assets and years of repayment.

Wesley Snipes was convicted on tax-related charges despite having advisors and accountants involved in his financial affairs.

In both cases, the public lesson was unmistakable:

The signature on the return belongs to the taxpayer.

The responsibility belongs to the taxpayer.

Hiring a professional is wise.

Abdicating oversight is not.

When Elena began meeting with her accountant before year-end instead of after, reviewing quarterly numbers, and asking forward-looking questions instead of backward explanations, something shifted.

She was no longer outsourcing awareness.

She was collaborating.

The calm business owner does not avoid tax conversations.

She engages in them.

She understands that her accountant is a partner — not a shield.

An accountant can guide.

An accountant can advise.

An accountant can interpret.

But no professional can care about your business more than you do.

When business owners expect their accountant to “handle everything,” they drift toward the next illusion.

Myth #4

The Write-Off Illusion

Perception:

The more I write off, the less I pay in taxes.

Reality:

Real and lasting tax savings come from structure, not just chasing deductions.

Carl loved the phrase “It’s a write-off.”

It made almost any purchase feel strategic.

New laptop? Write-off.

Dinner meeting? Write-off.

Conference in another state? Write-off.

Upgraded SUV? Write-off.

One evening over dinner with friends, he proudly said, “It doesn’t really matter. It’s a write-off anyway.”

He felt savvy. Ahead of the game. Like he had discovered a shortcut others had missed.

In his mind, deductions were equivalent to savings.

The logic felt simple:

If I deduct it, I don’t pay tax on it.

If I don’t pay tax on it, I save money.

But that logic was incomplete.

A deduction reduces taxable income.

It does not reimburse the full expense.

If Carl was in a combined federal and state tax bracket of 30 percent, a $10,000 “write-off” did not save him $10,000.

It saved him $3,000 in taxes.

He still spent $7,000.

Yet he walked away from the purchase feeling like he had “beaten the system.”

This illusion is common.

Business owners begin chasing deductions instead of evaluating profitability.

They justify purchases they might not otherwise make because “it lowers taxes.”

They confuse spending with strategy.

There is nothing wrong with legitimate deductions.

They exist for a reason.

But deductions are reactive.

Structure is proactive.

Carl rarely asked deeper questions:

Should this expense exist at all?

Is it generating revenue?

Is it improving efficiency?

Is there a more tax-efficient way to structure this purchase?

Instead, he focused on accumulating receipts.

By year-end, he had reduced “taxable income” alright.

But he had not necessarily increased net wealth.

The calm business owner understands something critical:

The goal is not to pay the least tax possible.

The goal is to build the strongest business possible within the law.

Those are not always the same thing.

There are only three ways to legitimately improve tax outcomes:

Increase efficiency.

Adjust structure.

Plan in advance.

Chasing deductions is not planning.

It is reacting.

When business owners focus obsessively on “what can I write off,” they often ignore larger structural decisions that create far greater impact:

Entity structure.

Compensation planning.

Timing of income and expenses.

Retirement contributions.

Asset classification.

Small deductions feel satisfying.

Structural decisions change trajectories.

Carl eventually realized that reducing taxable income was not the same as increasing retained earnings.

That realization shifted his mindset from opportunistic to intentional.

Write-offs are tools.

They are not strategy.

And confusing the two fuels the next myth.

Myth #5

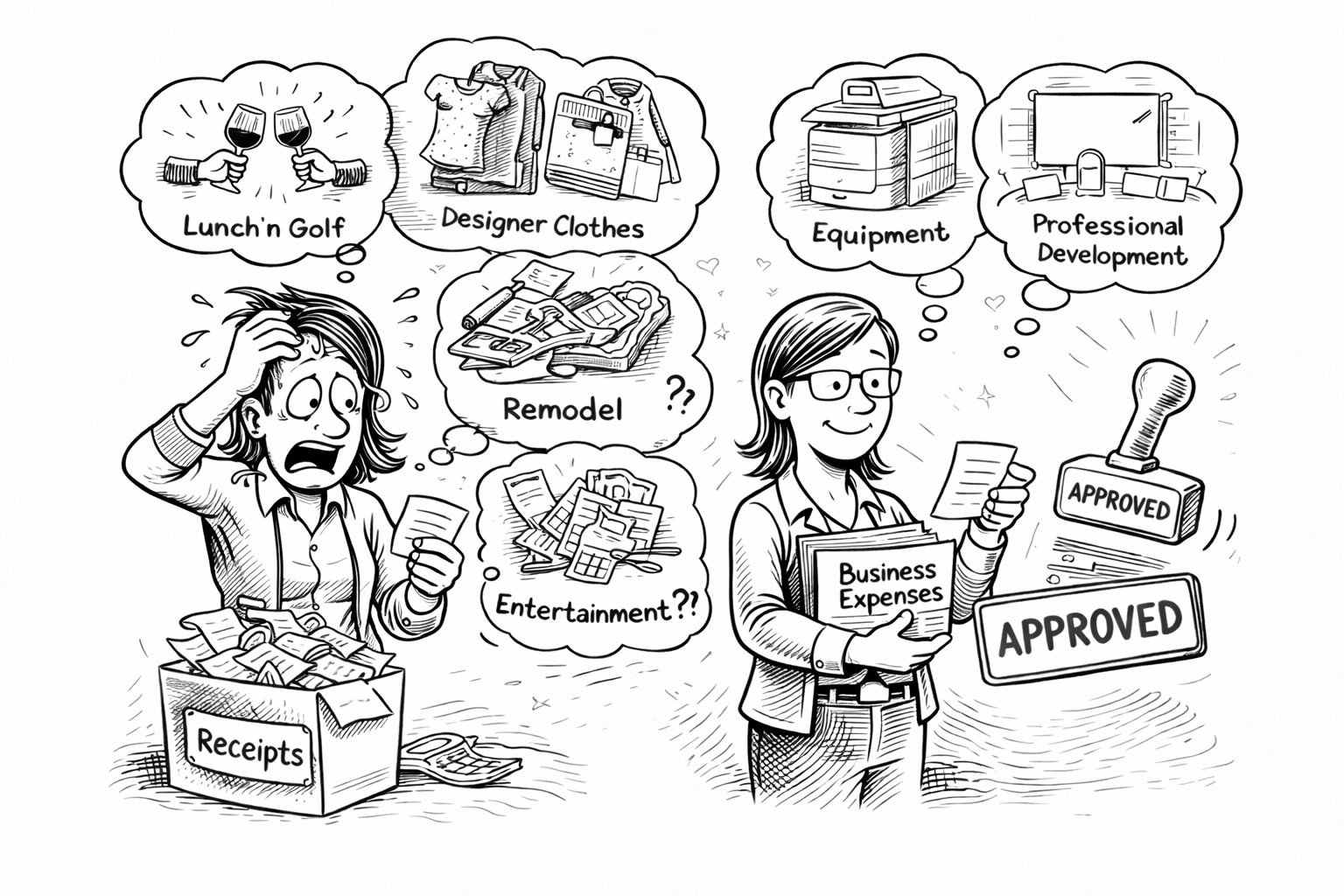

All “Business” Expenses Are Deductible

Perception:

If I classify an expense as business-related, it is deductible.

Reality:

An expense must be ordinary, necessary, properly documented, and defensible.

Maggie was careful.

Or at least she believed she was.

She had heard enough conversations about write-offs to know that “business expenses” reduced taxable income. So she made sure that anything even remotely connected to her business was categorized that way.

Home internet? Business.

Cell phone? Business.

Meals where business was mentioned? Business.

Clothing purchased for “professional presence”? Business.

After all, she was self-employed.

Everything touched her business in some way.

That was her reasoning.

What she did not understand was that labeling an expense does not make it deductible.

The IRS does not rely on labels.

It relies on standards.

For an expense to be deductible, it must generally meet specific criteria. It must be ordinary and necessary for the operation of the business. It must be properly documented. And it must be defensible if questioned.

“Ordinary” means common and accepted in your industry.

“Necessary” does not mean convenient.

It means appropriate and helpful for the business.

Those words matter.

Here is where the line becomes blurry.

A home internet bill may be partially deductible — but only the portion directly attributable to business use.

A vehicle may qualify for business deductions — but only based on documented business mileage, not total usage.

A meal with a client may qualify — but a dinner where business is casually discussed does not automatically convert a personal outing into a deductible expense.

Clothing is almost never deductible unless it is required, specialized, and not suitable for everyday wear.

Even home office deductions require clear qualification standards.

Borderline expenses are not automatically wrong.

But they are not automatically right either.

Intent does not override documentation.

Assumption does not override standards.

The problem is not usually dishonesty.

It is rationalization.

Business owners operate inside their companies every day. Conversations happen everywhere. Ideas are discussed at dinner tables. Work spills into weekends.

It becomes easy to say, “It’s all business.”

But tax law requires separation.

Clear boundaries protect credibility.

The calm business owner asks different questions:

Would this expense exist if the business did not?

Can I clearly document its business purpose?

Is there a reasonable allocation between personal and business use?

Would I feel comfortable defending this classification in writing?

If the answer is uncertain, the classification should be reconsidered.

This is not about fear.

It is about defensibility.

When deductions are ordinary, necessary, documented, and proportionate, they are powerful and legitimate.

When they are stretched, rounded up, or casually assigned, they create exposure.

Maggie eventually adjusted her mindset.

She stopped asking, “Can I write this off?”

She began asking, “Can I defend this?”

That shift alone reduced risk more than any deduction ever saved.

And when business owners blur the line between personal and business expenses, it often connects to a deeper structural issue — which leads directly into the next myth.

Myth #6

I’ll Incorporate Later

Perception:

I’m not big enough yet. Incorporation can wait.

Reality:

Business structure determines flexibility, liability separation, and future tax options. Restructuring later is often more costly than structuring properly at the start.

Javier had been running his business as a sole proprietor for three years.

Revenue was growing. Clients were steady. Cash flow was improving.

Friends had mentioned incorporating.

His accountant had casually suggested it.

But Javier always gave the same answer.

“I’m not big enough yet.”

To him, incorporation felt like something you did when you had a large team, a formal office, and a six-figure salary.

He saw it as a milestone.

Not a foundation.

So he waited.

And while he waited, several things quietly happened.

All business income flowed directly into his personal tax return.

As revenue increased, so did his marginal tax rate.

There was no ability to retain earnings inside the company structure.

There was no separation between personal and business liability.

There was no flexibility in how compensation could be structured.

And there was no long-term planning around distributions, retirement strategy, or risk insulation.

But because nothing had gone wrong, Javier assumed nothing was wrong.

That assumption is common.

Many business owners treat incorporation as a badge of success rather than a strategic decision.

But structure shapes options.

A sole proprietorship is simple.

It is also limited.

An incorporated entity creates additional compliance responsibilities. It requires bookkeeping discipline. It introduces corporate filings and administrative costs.

But it also creates:

Potential tax deferral opportunities.

Liability separation between business and personal assets.

More flexibility in compensation planning.

Clearer operational structure.

Incorporation is not always necessary immediately.

But postponing it without evaluation is not strategy.

It is avoidance.

When Javier finally incorporated, he realized something uncomfortable.

Had he structured earlier, he could have retained earnings during higher-income years, smoothed personal tax exposure, and separated certain risks.

Instead, restructuring required adjustments, legal filings, and transitional complexity.

Waiting had not been free.

It had been expensive in ways he did not see at the time.

The calm business owner does not incorporate emotionally.

He evaluates timing strategically.

He asks:

What are my growth projections?

What is my liability exposure?

What tax bracket trajectory am I on?

What flexibility might I need in three to five years?

Structure is not about ego.

It is about options.

When business owners treat incorporation as something to “do later,” they often delay decisions that affect every myth that follows.

And delayed structure leads directly into the next misunderstanding.

Myth #7

I Just Need to Make More Money

Perception:

If I increase revenue, tax problems and financial pressure will take care of themselves.

Reality:

Higher revenue without structural clarity often increases tax exposure and financial stress rather than reducing it.

Tasha was driven.

When expenses felt tight or taxes felt heavy, she had a simple solution:

“I just need to make more money.”

It sounded ambitious. Productive. Forward-thinking.

More clients.

More sales.

More revenue.

Problem solved.

And at first, it seemed to work.

Revenue increased.

But so did everything else.

Her taxable income rose sharply because she had not adjusted her withholding or estimated payments.

She hired contractors without reviewing classification standards.

She upgraded equipment without planning depreciation impact.

She increased advertising spend without measuring return.

Cash flow improved — temporarily.

Then quarterly tax payments arrived.

Then year-end adjustments hit.

Then surprise self-employment tax calculations surfaced.

Tasha was earning more… and feeling more pressure.

Revenue growth without structural planning amplifies every weakness in a business.

Higher income can push a taxpayer into a higher bracket.

It can increase exposure to additional taxes.

It can change filing requirements.

It can create compliance thresholds that did not previously apply.

Growth magnifies structure.

If the structure is strong, growth feels empowering.

If the structure is weak, growth feels overwhelming.

Tasha believed revenue solved problems.

What she eventually learned was this:

Revenue reveals problems.

More money flowing through a disorganized system does not create clarity.

It creates complexity.

More transactions.

More documentation.

More reporting requirements.

More scrutiny.

The calm business owner understands a different equation.

Revenue is fuel.

Structure is containment.

Fuel without containment creates fire.

Contained fuel creates propulsion.

Before chasing higher revenue, the disciplined business owner asks:

Is my bookkeeping current?

Are my estimated payments aligned with projected income?

Is my entity structure still appropriate?

Are compensation and distributions planned?

Growth is powerful.

But unmanaged growth can be destabilizing.

Tasha eventually shifted her focus.

Instead of asking, “How can I make more?”

She began asking, “Is my structure ready for more?”

That shift changed everything.

Because increasing revenue without structural clarity does not reduce tax stress.

It multiplies it.

And that leads directly into the next myth.

Myth #8

I Can Save Money and Simplify Reporting by Classifying a Worker as a Contractor

Perception:

I can decide whether someone is an employee or contractor based on what works best for my business.

Reality:

Classification is defined by the nature of the working relationship. Structure determines obligation, not preference.

Marcus was practical.

When his business began growing, he needed help. More hands. More capacity. More output.

Hiring employees felt complicated.

Payroll taxes.

Withholding.

Workers’ compensation.

Unemployment insurance.

So he chose what felt simpler.

“I’ll just pay them as contractors.”

No payroll setup.

No withholding calculations.

Just invoices and payments.

It seemed efficient.

And in the short term, it was.

But classification is not determined by convenience.

It is determined by control.

Marcus set the worker’s schedule.

He dictated how tasks were completed.

He supplied the tools.

He required exclusivity.

The relationship functioned like employment.

But it was labeled as contract work.

The IRS and state agencies evaluate classification using multiple factors, often centered around behavioral control, financial control, and the overall nature of the relationship.

It is not what you call the worker.

It is how the relationship operates.

When classification is incorrect, consequences can include:

Back payroll taxes.

Penalties.

Interest.

Retroactive benefits exposure.

What began as an attempt to “simplify reporting” can become an expensive correction.

Marcus did not intend to misclassify.

He intended to reduce complexity.

But reducing administrative burden does not override legal standards.

The calm business owner understands something critical:

Administrative simplicity is not the same as compliance simplicity.

Before determining classification, he asks:

Who controls the schedule?

Who controls how the work is performed?

Who provides tools and equipment?

Is the relationship ongoing or project-based?

Does the worker operate an independent business serving multiple clients?

These questions define status.

Not preference.

Not cost savings.

Not convenience.

When Marcus adjusted his structure properly, payroll felt more complex.

But his exposure decreased dramatically.

Clarity replaced assumption.

And risk decreased.

Worker classification is not a paperwork decision.

It is a structural one.

And misunderstanding structure leads directly into the next myth.

Myth #9

My Accountant Can Fix Everything at Year-End

Perception:

As long as I file on time, any bookkeeping issues can be cleaned up at tax season.

Reality:

Structure built throughout the year creates planning opportunities. Cleanup after the fact can only report what already happened.

Olivia considered herself responsible.

She met deadlines.

She kept receipts.

She hired a reputable accountant.

So she wasn’t worried.

Her system was simple.

Operate all year.

Sort it out in March.

Send everything to the accountant.

Problem handled.

Or so she believed.

Each December, her bookkeeping was incomplete. Some transactions were uncategorized. Certain expenses were grouped loosely. A few deposits required explanation.

But she reassured herself:

“My accountant will fix it.”

And the accountant did clean it up.

Reclassified expenses.

Requested missing documentation.

Adjusted totals.

Prepared the return.

Compliance was achieved.

But something critical was missing.

Planning.

Once the calendar year closes, most strategic options close with it.

Income has already been earned.

Expenses have already been incurred.

Entity choices have already been lived.

Compensation decisions have already been made.

An accountant can report history.

He cannot rewrite it.

Olivia assumed cleanup was optimization.

It was not.

Cleanup restores order to what already happened.

Strategy shapes what happens next.

Because her books were not reviewed quarterly, she missed opportunities to:

Adjust estimated payments.

Shift timing of certain expenses.

Evaluate retirement contributions before deadlines.

Revisit compensation structure.

By the time March arrived, the numbers were fixed.

The tax return reflected reality.

But reality had already been locked in.

The calm business owner understands a powerful distinction:

Tax preparation is backward-looking.

Tax planning is forward-looking.

They are not the same service.

They do not occur at the same time.

And they do not produce the same results.

When Olivia began reviewing her financial statements monthly and meeting with her accountant before year-end, the dynamic changed.

Questions became proactive instead of reactive.

Decisions became intentional instead of historical.

Her accountant stopped being a cleanup specialist.

He became a strategic partner.

Year-end is for reporting.

Mid-year is for shaping outcomes.

When business owners believe everything can be fixed at filing time, they delay the very conversations that create leverage.

And that leads directly into the next myth.

Myth #10

I Don’t Need to Worry About Taxes Until I’m Profitable

Perception:

If the business isn’t profitable yet, taxes aren’t a real concern.

Reality:

Tax obligations, reporting requirements, and structural decisions begin long before profitability. Ignoring them early can create costly consequences later.

Noah was in growth mode.

Revenue was coming in.

Expenses were high.

Marketing costs, software subscriptions, contractor payments, equipment purchases.

At the end of the year, his business showed little to no profit.

In his mind, that meant one thing:

“No profit. No tax problem.”

He focused entirely on growth.

Customer acquisition.

Brand visibility.

Product refinement.

Taxes felt like something successful companies dealt with.

He wasn’t “there” yet.

But profitability is not the only trigger for tax responsibility.

Self-employment tax can apply even when net profit is modest.

Quarterly estimated payments may still be required.

Sales tax obligations can arise regardless of overall profit.

Payroll filings must occur even if the company operates at a loss.

Reporting requirements do not wait for comfort.

Noah also overlooked something more subtle.

Even in lower-profit years, structural decisions matter.

How losses are treated.

Whether they are carried forward.

How expenses are categorized.

Whether an entity election might benefit future growth.

These decisions shape the next phase of the business.

Ignoring tax structure in early years often creates problems later:

Missed elections.

Incorrect filings.

Inconsistent bookkeeping.

Untracked basis calculations.

When growth finally accelerates, the foundation may already be unstable.

Noah eventually realized something important.

Tax planning is not reserved for profitable businesses.

It is foundational for growing businesses.

The calm business owner does not wait for profitability to build structure.

He builds structure in anticipation of it.

Because taxes are not triggered only by profit.

They are triggered by activity.

And misunderstanding activity leads directly into the next myth.

Myth #11

Filing an Extension Gives Me More Time to Pay

Perception:

If I file an extension, I don’t have to worry about payment until later.

Reality:

An extension may delay the filing deadline, but tax liabilities and interest calculations are not automatically postponed.

Ariana was organized.

She tracked deadlines.

She maintained a calendar.

She met client obligations on time.

But when April approached one year, she felt overwhelmed.

Her books needed final reconciliation.

A few documents were still missing.

There were questions she wanted clarified.

So she did what many business owners do.

She filed an extension.

Relief followed.

“Now I have more time.”

What Ariana misunderstood was subtle but significant.

An extension grants additional time to file the return.

It does not grant additional time to pay what is owed.

Taxes are generally due by the original deadline.

Interest begins accruing from that date.

Penalties may apply if sufficient payment is not made.

Filing paperwork is one timeline.

Payment is another.

Because Ariana assumed the extension covered both, she delayed calculating what she likely owed.

By the time the final return was prepared months later, interest had accumulated.

The amount was not catastrophic.

But it was unnecessary.

Extensions are legitimate tools.

They are useful when documentation is incomplete or clarification is needed.

But they are not shields against obligation.

The calm business owner understands this distinction:

An extension buys time for accuracy.

It does not buy time for avoidance.

Before filing an extension, Ariana eventually learned to ask:

What is my estimated liability?

Have I made sufficient estimated payments?

Should I submit an additional payment with the extension?

Those questions change the outcome.

When extensions are used strategically, they protect accuracy.

When they are used emotionally, they create delay.

Delay, in tax matters, often creates cost.

Understanding timelines — and the difference between filing and paying — prevents small misunderstandings from compounding.

And misunderstanding timelines often connects to the next myth.

Myth #12

Claiming a Home Office Will Trigger an Audit

Perception:

If I claim a home office deduction, I’m increasing my chances of being audited.

Reality:

Legitimate deductions, when properly calculated and documented, are part of the tax system. Avoiding valid claims out of fear can result in unnecessary overpayment.

Malcolm had a dedicated office in his home.

A separate room.

A desk.

Equipment.

Files.

It was used exclusively for business.

Yet every year at tax time, he hesitated.

“I’ve heard claiming a home office triggers an audit.”

The warning came from friends. From online forums. From vague stories that never included details.

So Malcolm avoided the deduction.

He absorbed the extra cost quietly.

Year after year.

What he misunderstood was simple.

The IRS does not initiate audits because of a single legitimate deduction.

It evaluates patterns, discrepancies, and statistical anomalies.

A properly calculated home office deduction that meets qualification standards is not suspicious. It is common.

The key word is properly.

To qualify, a home office must generally be used regularly and exclusively for business.

Regularly does not mean occasionally.

Exclusively does not mean primarily.

If the space doubles as a guest bedroom or family area, it likely does not qualify.

If it is clearly separated and used solely for business activity, it often does.

Malcolm’s office met the standards.

But fear overruled facts.

He worried that claiming the deduction would put him on a list.

In reality, failing to claim legitimate deductions does not reduce audit risk.

It increases overpayment.

The calm business owner does not inflate deductions.

He does not avoid legitimate ones either.

He calculates accurately.

He documents clearly.

He maintains reasonable allocations.

Home office deductions can be calculated using simplified methods or actual expense allocations. Both are permitted when applied correctly.

The issue is not the deduction.

The issue is defensibility.

When Malcolm reviewed the requirements carefully and maintained proper documentation, he realized something straightforward.

The deduction exists because many businesses operate from home.

It is built into the system.

Avoiding it out of fear did not reduce risk.

It only increased his tax bill.

Tax myths spread quickly.

Someone hears a story.

Someone repeats it.

Few verify it.

Fear moves faster than facts.

And that fear leads directly into the next myth.

Myth #13

Startup Costs Are Fully Deductible in the First Year

Perception:

All startup expenses can be deducted immediately once the business launches.

Reality:

Certain startup costs may be subject to limits or amortization rules. Structural planning before launch often determines how effectively those expenses are treated.

Vanessa was excited.

She had spent months planning her new business.

Before officially launching, she invested in branding, website development, consulting, legal fees, software subscriptions, market research, and early advertising.

By the time revenue began flowing, she had accumulated a substantial stack of receipts.

Her assumption was simple.

“These are all business expenses. I’ll deduct them this year.”

But startup costs are not always treated the same as operating expenses.

There is an important distinction between expenses incurred in the active operation of a business and those incurred before the business is officially up and running.

Certain startup expenses may be eligible for immediate deduction up to specific limits.

Others must be amortized over a number of years.

Some costs may fall into different categories altogether.

The treatment depends on timing, classification, and structure.

Vanessa had not considered that the date her business officially began operations mattered.

She had not evaluated whether certain pre-launch costs would be capitalized rather than expensed.

She had not asked whether forming an entity earlier might have changed how some expenses were handled.

None of her actions were reckless.

They were simply uninformed.

Startup energy often focuses on momentum.

Launch the product.

Build the brand.

Secure the clients.

Tax treatment feels secondary.

But early decisions shape future flexibility.

If expenses are misclassified, deductions may be delayed.

If timing is misunderstood, benefits may be reduced.

If records are incomplete, defensibility weakens.

The calm business owner approaches startup costs strategically.

Before launching, she asks:

When does my business officially begin operations?

How are my pre-launch expenses categorized?

Should certain purchases be structured differently?

Does my entity formation timing affect deductibility?

These questions do not slow momentum.

They strengthen it.

Startup costs are legitimate.

But legitimacy does not override structure.

Vanessa eventually learned that preparation before launch creates clarity after launch.

Excitement builds businesses.

Structure sustains them.

And misunderstanding startup structure leads directly into the final myth before the payoff.

Myth #14

Meals, Vehicles, and Common Expenses Are Fully Deductible

Perception:

If it’s related to business activity, it’s fully deductible.

Reality:

Many common expenses are subject to specific limitations, allocation rules, and documentation requirements. Overgeneralizing can lead to errors or missed optimization.

Victor ran a busy operation.

He met clients for lunch.

He drove to job sites.

He attended conferences.

He purchased equipment and tools throughout the year.

When tax time approached, he had one guiding principle:

“If it’s business-related, it’s deductible.”

That assumption felt reasonable.

After all, these expenses were connected to generating revenue.

But connection does not automatically equal full deductibility.

Meals, for example, are often deductible when they are ordinary and necessary business meetings. However, they are typically subject to percentage limitations under current tax rules. The deduction is legitimate, but it is not automatically one hundred percent.

Vehicles may qualify for deductions, but usually based on documented business mileage or a properly elected calculation method.

Travel expenses must meet clear business purpose standards.

Even common recurring costs may require allocation between personal and business use.

Victor’s mistake was not dishonesty.

It was oversimplification.

He assumed “business-related” meant “fully deductible.”

In reality, many expenses fall into categories with defined limits.

Some are partially deductible.

Some require allocation.

Some require detailed substantiation.

Without proper documentation, even legitimate expenses can be reduced or disallowed.

Victor had kept receipts.

But he had not consistently tracked mileage.

He had categorized vehicle costs broadly without reviewing which method was most appropriate.

He had assumed every client meal qualified at the same rate.

Nothing catastrophic occurred.

But small inaccuracies compound over time.

The calm business owner understands that common expenses are often the most scrutinized.

Not because they are suspicious.

Because they are frequent.

Before assuming full deductibility, Victor eventually began asking:

Is this expense subject to a percentage limitation?

Have I documented the business purpose clearly?

Should I use actual expenses or a standard mileage method?

Is there a required allocation between personal and business use?

These questions do not complicate business.

They clarify it.

Common expenses are powerful tools when handled correctly.

They become liabilities when handled casually.

Victor shifted from assumption to precision.

From broad labeling to documented allocation.

And that shift prepared him for the final transformation.

Because once the myths are dismantled, something else emerges.

Calm.

Myth #15

The Calm Business Owner (Not a Myth!)

These commonly believed tax myths were dismantled for one reason.

To give you peace.

Not theory.

Not technical jargon.

Peace.

Running a business already demands resilience.

Revenue pressure.

Client expectations.

Market uncertainty.

Operational complexity.

You do not need preventable tax anxiety layered on top of that weight.

Most tax stress is not created by the system.

It is created by misunderstanding.

By assumption.

By procrastination.

By fear.

Myths magnify tension.

Structure eliminates it.

The calm business owner is not someone who never receives a notice.

Not someone who never faces complexity.

Not someone who never makes a mistake.

The calm business owner understands the rules.

He builds structure before growth.

She maintains documentation before questions arise.

They plan before deadlines approach.

They review numbers before year-end locks them in.

They respond to procedures without panic.

Calm is not personality.

It is preparation.

It is not luck.

It is discipline.

It is not avoidance.

It is engagement.

The calm business owner does not chase write-offs.

He builds profit intentionally.

She does not fear audits.

She documents properly.

He does not blame the system.

He studies it.

She does not delay structure.

She implements it.

The difference between stress and steadiness is not income level.

It is understanding.

It is systems.

It is timing.

It is ownership.

You cannot eliminate every responsibility that comes with building something meaningful.

But you can eliminate unnecessary fear.

You can replace myths with clarity.

You can replace reaction with design.

And when structure is present, taxes become what they were always meant to be.

A system to be navigated.

Not a force to be feared.

That is the shift.

That is the discipline.

That is the identity.

That’s YOU!

The calm business owner.