Perception:

If I classify an expense as business-related, it is deductible.

Reality:

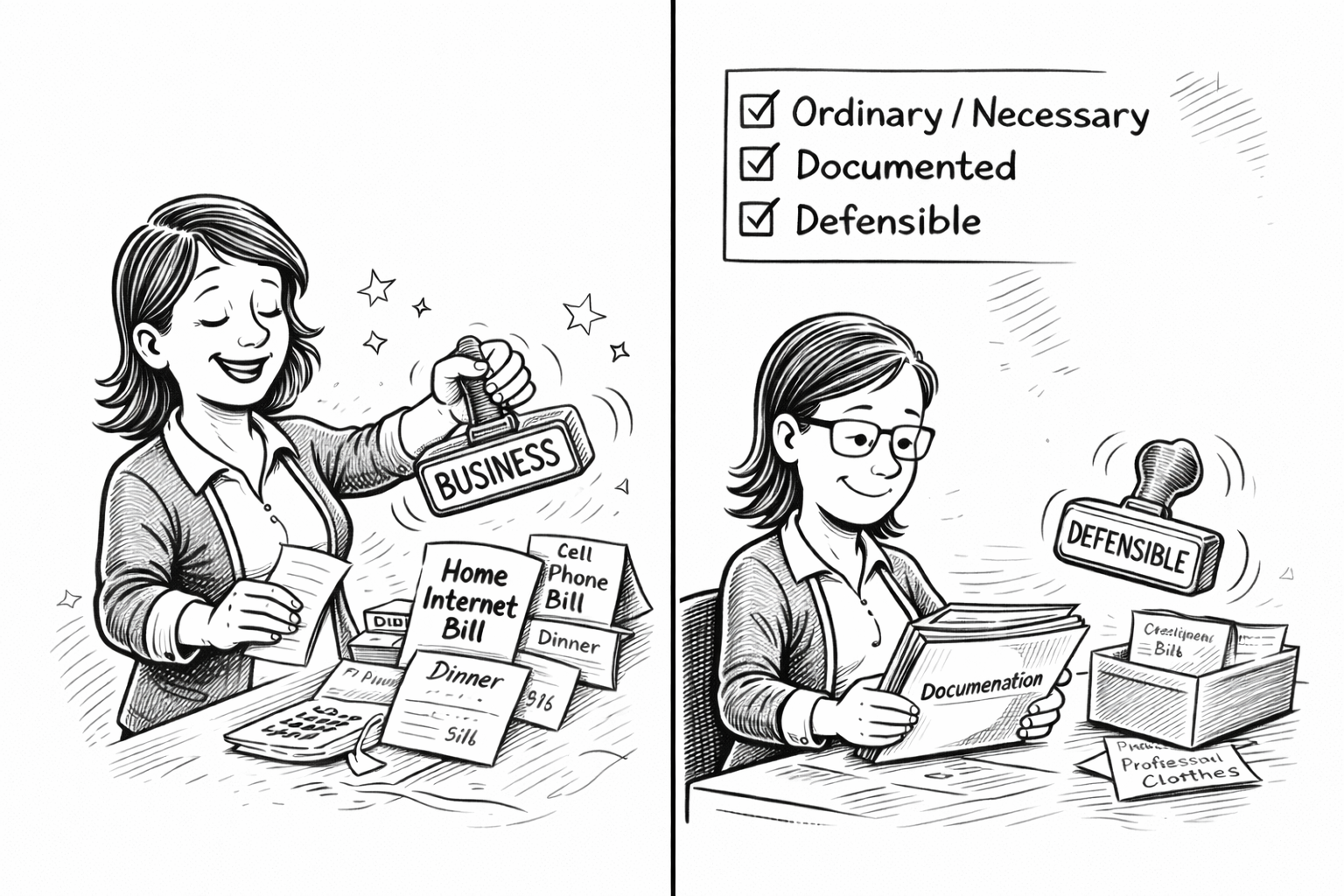

An expense must be ordinary, necessary, properly documented, and defensible.

Maggie was careful.

Or at least she believed she was.

She had heard enough conversations about write-offs to know that “business expenses” reduced taxable income. So she made sure that anything even remotely connected to her business was categorized that way.

Home internet? Business.

Cell phone? Business.

Meals where business was mentioned? Business.

Clothing purchased for “professional presence”? Business.

After all, she was self-employed.

Everything touched her business in some way.

That was her reasoning.

What she did not understand was that labeling an expense does not make it deductible.

The IRS does not rely on labels.

It relies on standards.

For an expense to be deductible, it must generally meet specific criteria. It must be ordinary and necessary for the operation of the business. It must be properly documented. And it must be defensible if questioned.

“Ordinary” means common and accepted in your industry.

“Necessary” does not mean convenient.

It means appropriate and helpful for the business.

Those words matter.

Here is where the line becomes blurry.

A home internet bill may be partially deductible — but only the portion directly attributable to business use.

A vehicle may qualify for business deductions — but only based on documented business mileage, not total usage.

A meal with a client may qualify — but a dinner where business is casually discussed does not automatically convert a personal outing into a deductible expense.

Clothing is almost never deductible unless it is required, specialized, and not suitable for everyday wear.

Even home office deductions require clear qualification standards.

Borderline expenses are not automatically wrong.

But they are not automatically right either.

Intent does not override documentation.

Assumption does not override standards.

The problem is not usually dishonesty.

It is rationalization.

Business owners operate inside their companies every day. Conversations happen everywhere. Ideas are discussed at dinner tables. Work spills into weekends.

It becomes easy to say, “It’s all business.”

But tax law requires separation.

Clear boundaries protect credibility.

The calm business owner asks different questions:

Would this expense exist if the business did not?

Can I clearly document its business purpose?

Is there a reasonable allocation between personal and business use?

Would I feel comfortable defending this classification in writing?

If the answer is uncertain, the classification should be reconsidered.

This is not about fear.

It is about defensibility.

When deductions are ordinary, necessary, documented, and proportionate, they are powerful and legitimate.

When they are stretched, rounded up, or casually assigned, they create exposure.

Maggie eventually adjusted her mindset.

She stopped asking, “Can I write this off?”

She began asking, “Can I defend this?”

That shift alone reduced risk more than any deduction ever saved.

And when business owners blur the line between personal and business expenses, it often connects to a deeper structural issue — which leads directly into the next myth.