Perception:

If it’s related to business activity, it’s fully deductible.

Reality:

Many common expenses are subject to specific limitations, allocation rules, and documentation requirements. Overgeneralizing can lead to errors or missed optimization.

Victor ran a busy operation.

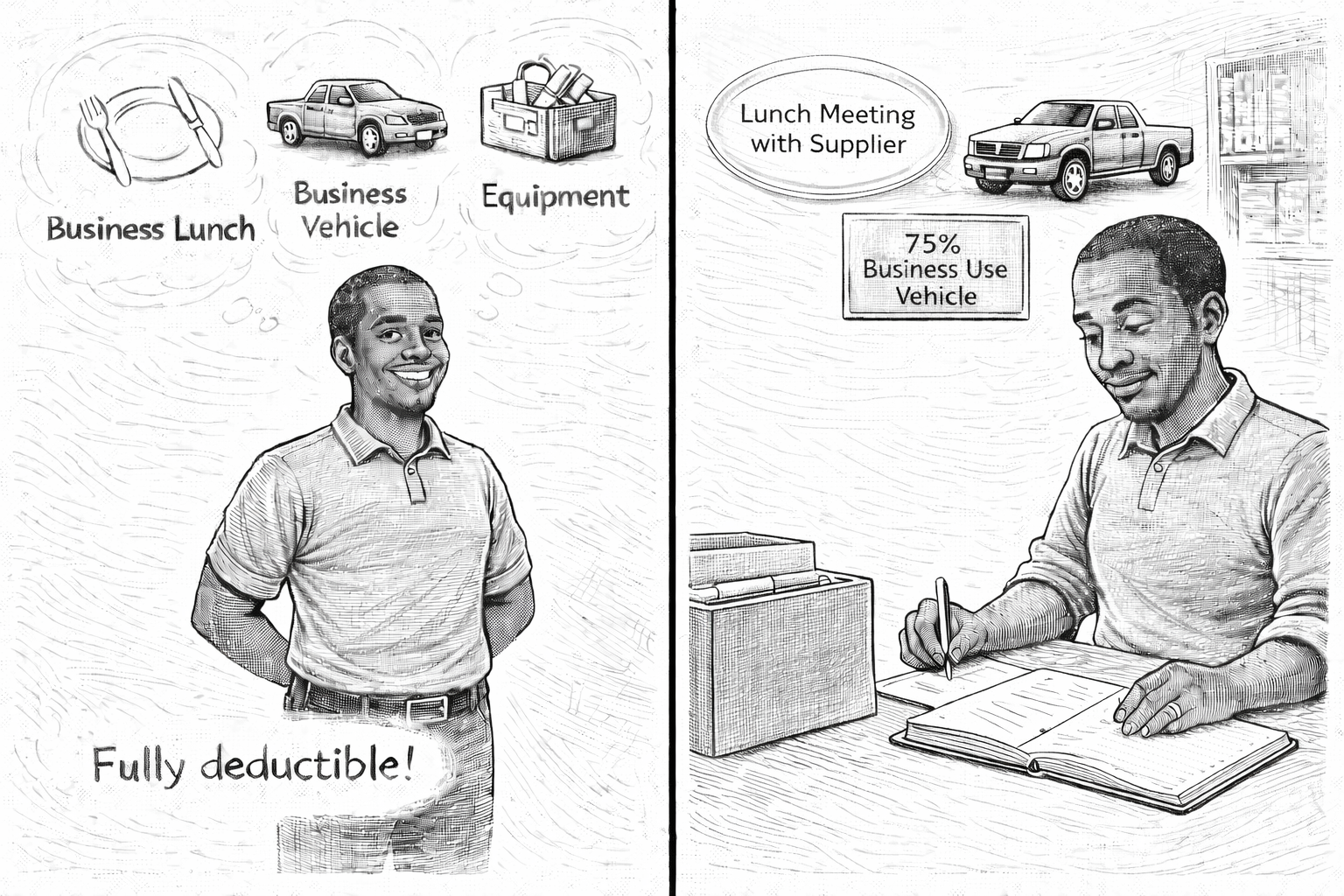

He met clients for lunch.

He drove to job sites.

He attended conferences.

He purchased equipment and tools throughout the year.

When tax time approached, he had one guiding principle:

“If it’s business-related, it’s deductible.”

That assumption felt reasonable.

After all, these expenses were connected to generating revenue.

But connection does not automatically equal full deductibility.

Meals, for example, are often deductible when they are ordinary and necessary business meetings. However, they are typically subject to percentage limitations under current tax rules. The deduction is legitimate, but it is not automatically one hundred percent.

Vehicles may qualify for deductions, but usually based on documented business mileage or a properly elected calculation method.

Travel expenses must meet clear business purpose standards.

Even common recurring costs may require allocation between personal and business use.

Victor’s mistake was not dishonesty.

It was oversimplification.

He assumed “business-related” meant “fully deductible.”

In reality, many expenses fall into categories with defined limits.

Some are partially deductible.

Some require allocation.

Some require detailed substantiation.

Without proper documentation, even legitimate expenses can be reduced or disallowed.

Victor had kept receipts.

But he had not consistently tracked mileage.

He had categorized vehicle costs broadly without reviewing which method was most appropriate.

He had assumed every client meal qualified at the same rate.

Nothing catastrophic occurred.

But small inaccuracies compound over time.

The calm business owner understands that common expenses are often the most scrutinized.

Not because they are suspicious.

Because they are frequent.

Before assuming full deductibility, Victor eventually began asking:

Is this expense subject to a percentage limitation?

Have I documented the business purpose clearly?

Should I use actual expenses or a standard mileage method?

Is there a required allocation between personal and business use?

These questions do not complicate business.

They clarify it.

Common expenses are powerful tools when handled correctly.

They become liabilities when handled casually.

Victor shifted from assumption to precision.

From broad labeling to documented allocation.

And that shift prepared him for the final transformation.

Because once the myths are dismantled, something else emerges.

Calm.