Before We Go Any Further… Read This First

Ten years ago, I fired my accountant.

My only regret?

I should have done it years earlier.

Every year, I did what most business owners do. I gathered my records, organized what I could, and handed everything over.

And every tax season, I would sit across from him behind his big oak desk and hear the same thing:

“Paul… you owe this much.”

To get to his office, I had to walk through a hallway lined with assistants. A dozen of them, all staring into their screens, all working on someone else’s books.

I remember thinking, this guy must be good.

He was busy. He was successful. People trusted him.

Including me… or at least I thought I did.

But every time I wrote that check, there was a question in the back of my mind:

Did he miss anything?

And if he did… how much is that costing me?

Then something happened. Something that should never happen.

He forgot to file my return.

Not delayed. Not complicated.

Forgot.

Of course, I confronted him. He apologized and said he would cover the penalty. But that wasn’t the point.

The question hit me like a brick:

If he could miss something that big… what else had he missed?

And more importantly… how much had it already cost me?

I’ve always been the kind of person who looks into things. If something doesn’t feel right, I don’t ignore it.

I dig.

So I started digging. I read, I studied, and I looked at what actually qualifies… and what gets missed.

And what I found shocked me.

Not a little.

A lot.

Over the years I worked with him, there were deductions that were never claimed, expenses that were never structured properly, and opportunities that were simply ignored.

Tens of thousands of dollars!

Gone.

Not because anything illegal happened. Not because anyone was trying to cheat the system.

But because no one was building my case.

That was the moment everything changed.

Because I realized something most business owners never do:

It’s not enough to hand your numbers over.

It’s not enough to “have an accountant.”

And it’s definitely not enough to assume everything is being handled.

If you don’t know what to look for, you won’t see it. You won’t track it. And at tax time… it’s gone.

Quietly.

Legally.

Permanently.

That’s why this exists.

This is not a list. Not theory. Not recycled advice.

This is a different way of looking at your numbers… so you can start seeing what was always there—but never captured.

About the Author, Why This Book Matters & How to Use This Book

Paul Neill is an entrepreneur, teacher, and author with over 45 years of experience building and operating small businesses across multiple industries.

Over the course of his career, he has worked alongside business owners who are skilled in their craft yet often uncertain about the financial and tax consequences of everyday decisions.

Paul is known for explaining complex subjects in clear, direct language. His work emphasizes disciplined systems that reduce risk, eliminate unnecessary stress, and support strong, defensible records.

As Founder of Tax Ready Ledger Co., he helps business owners maintain clean, consistent books that support confident tax filings and sound business judgment.

The Tax Deduction Detective reflects his conviction that most missed deductions are not hidden. They are simply never structured, captured, or recognized.

When you learn to see them, you don’t just reduce taxes… you stop leaving money behind..

Why This Book Matters

Most business owners don’t lose money because they’re careless.

They lose it because no one ever showed them what to look for.

They work hard. They generate income. They trust that when tax time comes, everything will be handled.

And for the most part, it is.

But what gets handled… is only what was captured.

And what gets captured is often incomplete.

Not because anything is being done wrong.

But because no one is building the case.

This book exists to change that.

This is not a list of deductions.

It’s a different way of seeing your business.

Because every deduction you’ve ever missed was never really hidden.

It was simply never structured, tracked, or recognized for what it actually was.

That’s the difference.

When you begin to see your numbers differently, you start to recognize what was always there.

Expenses that support the business.

Costs that should reduce your taxable income.

Opportunities that don’t come from doing more… but from seeing clearly.

This is what tax intelligence looks like in real life.

Not shady.

Not risky.

Not complicated.

Just accurate, structured, and complete.

And when that happens, something shifts.

You stop guessing.

You stop wondering what was missed.

And you start operating with clarity.

How to Use This Book

This is not a book you read once and put away.

It’s something you come back to.

Each section stands on its own. You don’t need to read it in order. Start with what applies to you right now.

As you go through it, don’t try to absorb everything at once. The value is not in memorizing rules. It’s in recognizing patterns.

You’ll start to notice how certain expenses show up in your business.

How they are currently being handled.

And how small changes in classification, documentation, or timing can change the outcome.

Some sections will feel immediately relevant.

Others may not apply yet.

That’s fine.

The goal is not to use everything.

The goal is to see clearly when something does apply… so nothing gets missed.

Then there is the final section of this book.

The deep dive.

This is not something you read from beginning to end.

It is a reference system.

A way to quickly identify expenses that may already exist in your business but have never been fully recognized, classified, or captured.

As your awareness grows, this section becomes more valuable.

You begin to see connections.

You begin to recognize patterns faster.

And you start to identify opportunities you would have overlooked before.

Over time, this becomes a way of thinking.

Not just at tax time…

But throughout the year.

🕵️♂️ #1: Marketing & Advertising

The Expense That Pays You Back… and Then Pays You Again at Tax Time

There are very few deductions where the same dollar does two jobs.

Marketing is one of them.

It brings in the business… and it reduces what you’re taxed on.

A realtor runs ads every month to stay in front of buyers and investors.

A personal injury lawyer pays for high-value leads in a competitive market.

A plumber invests in local service ads so the phone rings consistently.

An online coach spends anywhere from a few thousand to tens of thousands a month to keep leads flowing.

Different businesses. Same reality.

Money goes out… business comes in.

From a tax standpoint, marketing and advertising is clean. It is 100% deductible. If $25,000 is spent to generate business, that $25,000 reduces the income being taxed.

That part is simple.

What is not simple… and where most people leave money behind… is how that spending is structured, captured, and expanded.

One business owner runs ads, pays for creative work, prints materials, sponsors events, and never sees the full picture. Charges are scattered across cards. Some are buried in subscriptions. Some are forgotten entirely. At year end, they guess.

Another business owner runs the exact same activity but treats marketing like a system. Every dollar that touches visibility flows through the business. Ads, creative, printing, lead services, agency work, sponsorships. All recorded. All labeled. Nothing mixed. Nothing lost.

Same spending. Different outcome.

Now the deduction is complete.

That is the baseline.

Now we move to what most people miss.

A realtor hosts a private dinner. Not a casual evening. A targeted event. Investors. Buyers. People capable of doing real deals. The cost is significant. If this is treated as a simple meal, it gets limited. If it is structured as a client acquisition event, documented properly, followed up with actual business activity, it becomes a marketing expense.

Same dinner. Same cost.

Different classification. Different result.

What makes it hold is intent and proof. Invitations, who attended, what business came from it.

🕵️♂️ Deduction

Client acquisition event structured as marketing

🔍 Missed Evidence:

No record of attendees or follow-up activity

⚠️ Red Flag:

Appears to be a personal or social dinner

💡 Defense Strategy:

Maintain guest list, business purpose, and tie outcomes to real opportunities or deals

Another example.

A business owner hires a videographer, editor, and runs content shoots throughout the year. Many treat this as a general contractor expense and it disappears into the noise.

Structured properly, this is marketing.

The content is used to attract clients, run ads, build funnels, generate leads.

Now the expense is not just recorded. It is clearly positioned as client acquisition activity.

🕵️♂️ Deduction

Content production classified as marketing

🔍 Missed Evidence:

No proof content was used to promote the business

⚠️ Red Flag:

Looks like a personal or creative project

💡 Defense Strategy:

Keep published content, campaign links, and platform usage tied to business activity

Another move that rarely gets used properly.

A strong year. Income is high. Taxes will follow.

Instead of slowing down, the business leans into marketing before year end. Campaigns are funded. Retainers are paid. Media is booked. Real campaigns, real activity.

Cash goes out in the current year.

The deduction follows.

Same money that would have been spent anyway… now working in a year where it matters more.

🕵️♂️ Deduction

Prepaid marketing tied to active campaigns

🔍 Missed Evidence:

No invoice or campaign schedule tied to payment

⚠️ Red Flag:

Looks like an artificial expense to reduce income

💡 Defense Strategy:

Document campaign scope, timing, and execution plan before year end

There is also the small detail that adds up to large numbers.

Lead services.

A lawyer pays monthly for inbound leads. A contractor pays for referral platforms. A consultant pays for listing visibility.

When these are tracked clearly as marketing, they strengthen the category and make the full acquisition cost visible.

When they are scattered, they disappear into general expense.

Same cost. Less clarity. Weaker position.

🕵️♂️ Deduction

Lead generation and referral services

🔍 Missed Evidence:

Expenses buried in general or misc categories

⚠️ Red Flag:

No clear connection to acquiring business

💡 Defense Strategy:

Track all lead-related costs under marketing with clear business purpose

Local sponsorships are another quiet opportunity.

A business sponsors a community event, a local team, or a public function. If there is clear business exposure, name placement, visibility tied to the business, this is not a donation.

It is advertising.

That distinction matters.

🕵️♂️ Deduction

Local sponsorship classified as advertising

🔍 Missed Evidence:

No proof of business visibility or promotion

⚠️ Red Flag:

Appears to be a charitable contribution

💡 Defense Strategy:

Document logo placement, signage, and public exposure tied to the business

Where this breaks down is predictable.

Expenses mixed with personal activity. No clear business purpose. No record of intent. No follow-through. No tracking.

And at that point, even legitimate spending becomes weak.

Not because it shouldn’t qualify… but because it cannot be supported.

The opportunity here is not hidden.

Every business that wants clients spends money to get them.

The difference is whether that spending is treated casually… or deliberately.

When it is deliberate, two things happen.

The business grows.

And the full cost of creating that growth is properly recognized.

That is how this category is meant to work.

Not just as an expense.

But as a system.

🕵️♂️ #2: Contractors / Fulfillment

The Expense That Builds Income Without Building Payroll

Some expenses grow with your business.

Others limit it.

Contractors are different.

They expand what you can deliver without tying you down.

A marketing agency hires designers, editors, and media buyers to fulfill client work.

An online coach pays setters, closers, and support staff to handle sales and onboarding.

A consultant brings in specialists to execute parts of a project.

A service business outsources bookkeeping, admin, or technical work to keep operations moving.

Different roles. Same function.

Work gets done… without adding employees.

From a tax standpoint, contractor and fulfillment costs are clean. They are 100% deductible. If $80,000 is paid out to contractors to deliver services, that $80,000 reduces the income being taxed.

Simple.

What is not simple, and where most people leave money behind, is how those payments are structured, tracked, and supported.

One business owner pays a mix of helpers throughout the year. Some by transfer. Some by check. Some in cash. No agreements. No clear records. At year end, they try to piece it together. Some payments are missed. Some cannot be supported. Some should have been reported and weren’t.

The deduction weakens.

Another business owner runs the same activity through a system. Every payment goes through the business. Every contractor is identified. Every role is tied to actual work performed. There are agreements. There are invoices. There are records.

At year end, nothing is guessed.

The deduction holds.

Same spending. Different outcome.

A business owner does everything themselves. Delivery, admin, follow-ups, support. Income is capped because time is capped.

Then they bring in help. Not randomly, but intentionally.

A setter handles inbound leads.

A closer handles sales calls.

An assistant handles onboarding.

Revenue increases. The cost of producing that revenue increases with it.

That cost is fully deductible.

🕵️♂️ Deduction

Contractor-based fulfillment

🔍 Missed Evidence:

No invoices or agreements tied to payments

⚠️ Red Flag:

Appears informal or undocumented

💡 Defense Strategy:

Maintain contracts, invoices, and clear records of services provided

A business owner hires help but mixes personal and business activity. A contractor edits videos, some for business, some personal. An assistant handles both business tasks and personal errands.

Now the expense is blurred.

Part of it holds. Part of it does not.

🕵️♂️ Deduction

Mixed-use contractor expenses

🔍 Missed Evidence:

No separation between business and personal work

⚠️ Red Flag:

Entire expense appears inflated or unsupported

💡 Defense Strategy:

Clearly separate business tasks and allocate only the business portion

Another business owner pays contractors irregularly. One month here. One month there. No defined scope. No consistency. The expense exists, but it lacks structure.

Another business owner sets defined roles, recurring payments, and clear deliverables. Now the expense is predictable, traceable, and fully tied to business activity.

🕵️♂️ Deduction

Structured contractor payments

🔍 Missed Evidence:

No defined scope or recurring structure

⚠️ Red Flag:

Appears casual or non-business in nature

💡 Defense Strategy:

Use consistent payment schedules and defined roles

A business owner hires employees too early. Payroll taxes increase. Administrative burden increases. Flexibility disappears.

Another business owner uses contractors where appropriate. Work gets done. Costs remain tied to production. The expense scales with the business.

🕵️♂️ Deduction

Contractor classification

🔍 Missed Evidence:

No clear distinction between contractor and employee roles

⚠️ Red Flag:

Worker appears to function as an employee

💡 Defense Strategy:

Ensure independence, defined scope, and proper working relationship

Another situation shows up at year end.

Payments were made. Work was done. But required reporting was ignored. No W-9 on file. No 1099 issued where required.

Now the deduction is exposed.

Another business owner collects W-9s up front, issues 1099s properly, and keeps everything aligned.

Now the deduction is not just valid.

It is defensible.

🕵️♂️ Deduction

Contractor compliance

🔍 Missed Evidence:

Missing W-9 or 1099 filings

⚠️ Red Flag:

Payments cannot be tied to a legitimate contractor relationship

💡 Defense Strategy:

Collect W-9s and issue 1099s where required

Contractors scale with the business. When revenue increases, fulfillment increases. When business slows, costs adjust.

The expense follows the activity.

And the deduction follows the expense.

Where this breaks down is predictable. Cash payments with no records. No agreements. No separation between personal and business tasks. No compliance on required filings.

At that point, even legitimate expenses become weak.

But when it is structured properly, contractors do more than help you grow.

They create a system where income expands and the cost of producing that income is fully recognized.

That is how this category is meant to work.

Not as random help.

But as structured fulfillment.

🕵️♂️ #3: Travel (Away From Tax Home)

When Your Business Moves… The Costs Move With It

Travel is one of the few deductions that feels natural.

You go somewhere to do business, you spend money to make that happen, and that cost follows the business.

A consultant flies out to meet a client.

A contractor spends a few days on a job in another city.

A coach attends an event or works with clients outside their area.

A service provider takes work that requires being away from home.

Nothing complicated about it.

You left your base to do business.

That’s the starting point.

When that happens, the major costs fall into place.

Flights.

Hotels.

Transportation.

These are part of doing the work, not extras.

They reduce what you’re taxed on because they are directly tied to earning the income.

Where people get tripped up isn’t in the travel itself.

It’s in overthinking it… or under-recording it.

One business owner takes a trip, uses their business card, keeps the basic receipts, and moves on.

At year end, everything is there.

Clean enough. Complete enough.

The deduction works exactly as it should.

Another business owner takes the same trip but pays for things in different ways, forgets a few items, doesn’t keep track of where money went.

Now the total is smaller than it should be.

Not because the expenses weren’t valid…

but because they weren’t captured.

That’s where the real loss happens.

Not in the rules.

In the gaps.

🕵️♂️ Deduction

Business travel away from your home base

🔍 Missed Evidence:

Expenses paid but never recorded or remembered

⚠️ Red Flag:

Travel activity exists but very little is reported

💡 Defense Strategy:

Use one card, keep receipts, and let the record build naturally

Now let’s talk about what most people quietly wonder about.

You go on a business trip and add a day or two.

You bring your spouse.

You do some sightseeing.

This is normal.

It happens all the time.

The presence of personal time does not erase the business purpose of the trip.

If the trip was taken for real business, the core travel cost still stands.

Flights don’t suddenly become personal just because you stayed an extra day.

Hotels and daily costs can vary depending on how things are handled, but the idea that everything collapses the moment you enjoy part of the trip is not how real life works.

🕵️♂️ Deduction

Business trip with added personal time

🔍 Missed Evidence:

No clear reason for the business portion of the trip

⚠️ Red Flag:

Trip appears mostly personal with vague business intent

💡 Defense Strategy:

Make sure the business purpose is real and obvious

Another common situation.

You attend an event, conference, or meet with clients while away.

You don’t need a detailed report.

But having something simple, a registration, confirmation, a few notes, even emails, gives the trip a clear business anchor.

That’s usually more than enough.

🕵️♂️ Deduction

Event or client-based travel

🔍 Missed Evidence:

No trace of why the trip happened

⚠️ Red Flag:

Travel with no visible connection to business

💡 Defense Strategy:

Keep simple proof of attendance or meetings

There’s also the practical side.

Travel adds up quickly.

Flights, hotels, rides, small daily costs.

Individually, they don’t seem like much.

Together, they become significant.

And if they’re not tracked as they happen, they fade.

🕵️♂️ Deduction

Accumulated travel expenses

🔍 Missed Evidence:

Small expenses forgotten over time

⚠️ Red Flag:

Travel activity doesn’t match reported totals

💡 Defense Strategy:

Capture expenses as they happen so nothing gets left behind

The real advantage of travel as a deduction is that it grows naturally with your business.

More opportunities.

More clients.

More movement.

And with that movement comes legitimate cost.

That cost reduces what you’re taxed on without any special maneuvering.

Where this goes wrong is not complexity.

It’s neglect.

Forgetting to track.

Mixing everything together.

Relying on memory instead of simple records.

But when handled the way most real businesses actually operate…

Travel doesn’t need to be perfect.

It just needs to be real.

And when it is, it works exactly the way it’s supposed to.

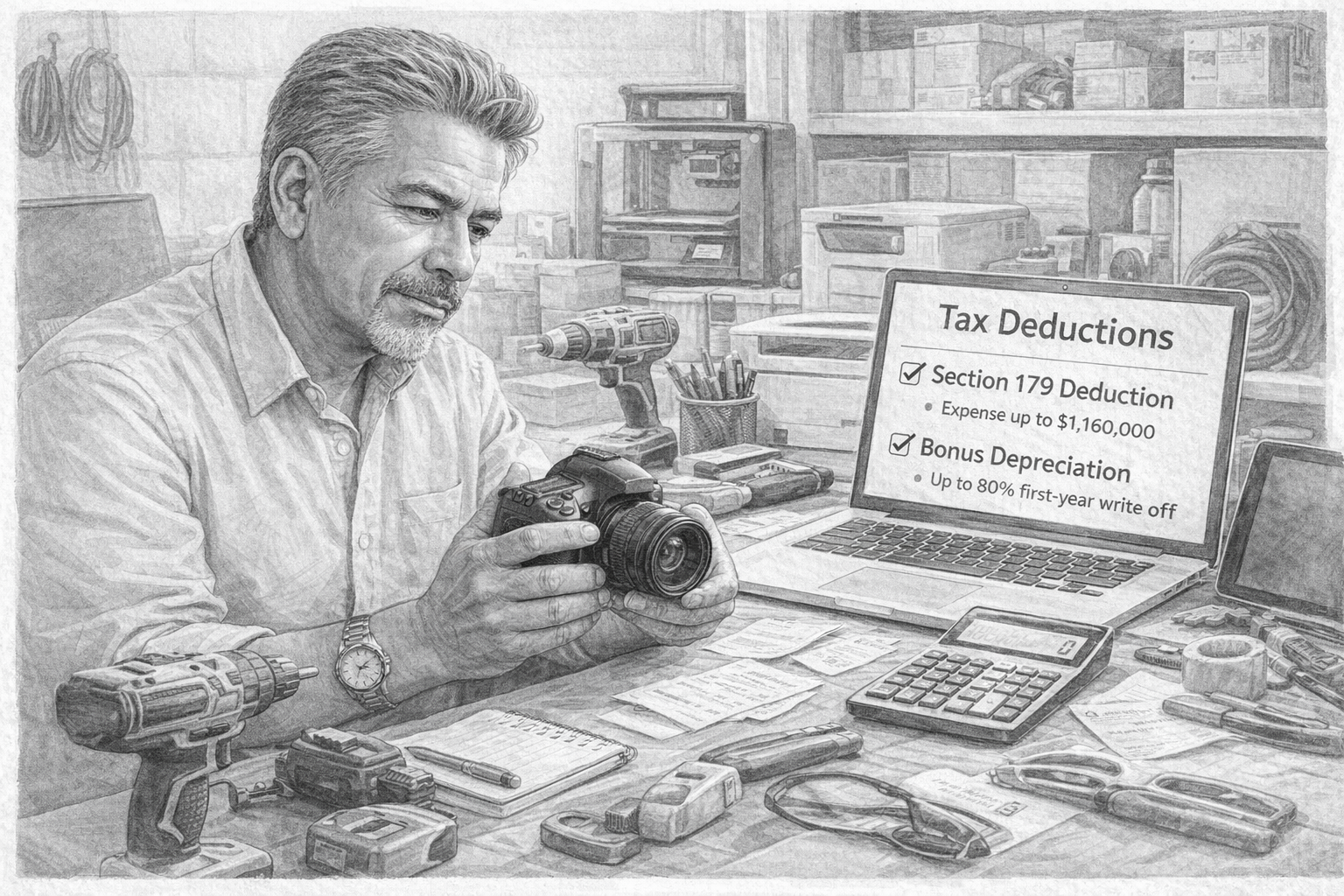

🕵️♂️ #4: Asset Expensing

When the Cost Hits Now… Not Later

Some purchases feel like investments.

Equipment.

Tools.

Technology.

They help you produce income, but they don’t disappear after one use.

That’s where this category lives.

A consultant buys a new laptop to run their business.

A videographer invests in cameras and editing equipment.

A contractor purchases tools needed to complete jobs.

An online business upgrades computers, lighting, or production gear.

These are not daily expenses.

They are assets.

And how they are handled changes the timing of the deduction.

One business owner buys equipment and spreads the deduction over several years without thinking much about it.

The expense is recognized slowly.

The tax benefit follows the same pace.

Another business owner buys the same equipment but expenses it in the year it was purchased.

Now the full cost reduces income immediately.

Same purchase.

Different timing.

Different result.

🕵️♂️ Deduction

Asset expensed in the year of purchase

🔍 Missed Evidence:

No clear record of when the asset was placed into service

⚠️ Red Flag:

Expense timing does not match actual usage

💡 Defense Strategy:

Document purchase date and when the asset began being used for business

A business owner upgrades equipment during a strong year.

Income is high. Taxes will follow.

The purchase is made before year end, and the full cost is recognized in that same year.

The equipment is already needed.

The timing simply aligns the expense with the income.

Another business owner waits until the following year.

The same purchase still happens.

But the deduction lands in a lower-income year, where it has less impact.

🕵️♂️ Deduction

Timing of asset purchase

🔍 Missed Evidence:

No connection between purchase timing and business use

⚠️ Red Flag:

Expense appears rushed or unrelated to business activity

💡 Defense Strategy:

Ensure the asset is actually needed and placed into service within the year

A business owner buys equipment that is used partly for business and partly for personal use.

Everything is claimed as business.

That does not hold.

Another business owner uses the same equipment but recognizes only the portion tied to business activity.

Now the deduction reflects reality.

🕵️♂️ Deduction

Partial business use of assets

🔍 Missed Evidence:

No distinction between personal and business use

⚠️ Red Flag:

100% business claim on mixed-use asset

💡 Defense Strategy:

Allocate based on actual business use and keep a reasonable basis for that split

A business owner makes several smaller purchases throughout the year.

Each one feels minor.

Individually, they don’t stand out.

Together, they represent a meaningful amount.

Some are tracked. Some are not.

The total gets diluted.

Another business owner captures each purchase as it happens.

Nothing is too small to record.

At year end, the full picture is there.

🕵️♂️ Deduction

Accumulated equipment purchases

🔍 Missed Evidence:

Small purchases not recorded consistently

⚠️ Red Flag:

Business activity suggests more equipment than reported

💡 Defense Strategy:

Record purchases as they occur so the full amount is recognized

A business owner replaces equipment that is essential to operations.

The purchase is not optional.

It keeps the business running.

The cost reflects that reality.

Another business owner delays necessary upgrades.

Work slows. Efficiency drops. The expense still comes later, but the business has already absorbed the cost in other ways.

The deduction exists either way.

But the timing changes how it works for you.

🕵️♂️ Deduction

Replacement of business-critical equipment

🔍 Missed Evidence:

No clear link between the asset and business use

⚠️ Red Flag:

Purchase appears discretionary or unrelated

💡 Defense Strategy:

Tie the asset directly to business activity and function

Assets are part of growth.

As the business expands, better tools are needed.

Better tools cost more.

And when those costs are handled properly, they reduce the income being taxed in a meaningful way.

Where this breaks down is not complexity.

It’s a disconnect.

Purchases made without being recorded.

Business use not clearly understood.

Timing ignored.

At that point, the deduction weakens.

But when handled the way real businesses operate…

The purchase is made because it is needed.

It is used in the business.

And the cost is recognized in a way that reflects that reality.

That is how this category is meant to work.

Not as a technical rule.

But as a direct reflection of how a business invests in itself.

🕵️♂️ #5: Income Timing

When You Get Paid Matters Just As Much As What You Earn

Most people focus on how much they make.

Fewer pay attention to when they make it.

And that timing quietly changes everything.

A consultant finishes a project in late December.

An online coach closes sales near year end.

A service provider sends invoices in the final weeks of the year.

The work is done.

The income is real.

But the moment it lands can shift the tax result.

One business owner sends invoices immediately and collects payment before year end.

That income is now part of the current year.

It gets taxed with everything else earned.

Another business owner finishes the same work but sends the invoice at the beginning of the next year.

Nothing artificial. No delay in the work itself.

Just a shift in when the income is received.

Now that same income falls into the following year.

Same work.

Different timing.

Different result.

🕵️♂️ Deduction

Income received in a later period

🔍 Missed Evidence:

No clear distinction between when work was completed and when payment was received

⚠️ Red Flag:

Income appears to be intentionally hidden or redirected

💡 Defense Strategy:

Ensure timing reflects normal business flow and actual receipt of payment

Another situation shows up near the end of a strong year.

Business is good. Revenue is high.

Payments are coming in quickly.

Everything looks positive… until the tax side catches up.

One business owner continues collecting aggressively through the final days of the year.

Income stacks up.

Taxes follow.

Another business owner slows the intake slightly.

Projects are scheduled into the new year.

Invoices are timed naturally with that schedule.

The work continues.

The income shifts.

🕵️♂️ Deduction

Controlled receipt of income

🔍 Missed Evidence:

No connection between business activity and timing of payments

⚠️ Red Flag:

Unusual or inconsistent payment patterns

💡 Defense Strategy:

Keep timing aligned with how work is actually scheduled and delivered

Now look at the other side.

Expenses.

A business owner knows certain costs are coming.

Software renewals.

Marketing campaigns.

Equipment purchases.

They wait until the next year.

The expense still happens.

But it lands later.

Another business owner handles those same costs before year end.

Nothing forced. Nothing unnecessary.

Just moving forward with what was already needed.

Now the expense reduces the current year’s income.

🕵️♂️ Deduction

Timing of expenses

🔍 Missed Evidence:

No link between expense timing and business need

⚠️ Red Flag:

Expense appears rushed with no clear purpose

💡 Defense Strategy:

Ensure expenses are legitimate and tied to actual business activity

A business owner receives advance payments.

Clients pay upfront for services that will be delivered later.

The money is in the account.

The question becomes when it is recognized.

Handled properly, the timing reflects how and when the service is actually delivered.

Handled loosely, everything gets pulled into one period without thought.

🕵️♂️ Deduction

Advance payments and timing

🔍 Missed Evidence:

No clarity on when services are delivered

⚠️ Red Flag:

Income recognition does not match business activity

💡 Defense Strategy:

Keep payment timing aligned with how services are performed

Another pattern shows up in everyday activity.

A business owner sends invoices randomly.

Some go out immediately. Some are delayed without reason.

Payments come in unpredictably.

There is no control.

Another business owner follows a rhythm.

Work is completed.

Invoices follow a consistent pattern.

Payments align with that flow.

Now the timing is not forced.

It is simply structured.

🕵️♂️ Deduction

Consistent income flow

🔍 Missed Evidence:

No pattern in billing or payment timing

⚠️ Red Flag:

Irregular spikes that don’t match business activity

💡 Defense Strategy:

Maintain a consistent invoicing approach tied to actual work

Income timing is not about manipulation.

It is about awareness.

The work happens.

The income follows.

But when that income is received can shift how it is taxed.

Handled naturally, within the rhythm of the business, it becomes a quiet advantage.

Ignored, it becomes something that controls you instead of the other way around.

That is how this category is meant to work.

Not as a trick.

But as timing that reflects how real business actually operates.

🕵️♂️ At Tax Ready Ledger Co., we don’t just track your numbers… we structure them so they make sense, hold up, and work in your favor. Learn more at taxreadylc.com.

🕵️♂️ #6: Vehicle

When Your Driving Becomes Part of the Business

A vehicle is one of the most commonly used tools in a service business.

It doesn’t feel like a “business asset” at first.

It just feels like how you get around.

A realtor drives to show properties.

A contractor moves between job sites.

A consultant travels to meet clients.

A service provider runs errands, picks up materials, and handles day-to-day operations.

The movement is constant.

And when that movement is tied to business, the cost follows.

Fuel.

Maintenance.

Repairs.

Insurance.

All of it becomes part of doing the work.

From a tax standpoint, there are two common ways this is handled.

Some business owners track mileage.

Others track actual expenses.

Both work.

The difference is not which one exists.

It’s which one reflects reality better.

One business owner drives all year for business and never tracks anything.

At year end, they try to estimate.

Most of it is lost.

Another business owner uses a simple mileage app.

They drive as usual.

The app runs quietly in the background and records trips automatically.

No guesswork. No reconstruction.

Apps like MileIQ, Everlance, and QuickBooks Mileage make this almost effortless.

Now the business use is clear without adding work.

🕵️♂️ Deduction

Business mileage

🔍 Missed Evidence:

No record of business trips or usage

⚠️ Red Flag:

Vehicle expenses claimed with no supporting pattern

💡 Defense Strategy:

Use a simple mileage app or log to consistently track business driving

Another business owner uses the same vehicle for both business and personal use.

Everything is claimed as business.

That does not hold.

Another business owner uses the same vehicle but lets the tracking tell the story.

Business trips are recorded. Personal trips are ignored.

Now the deduction reflects what actually happened.

🕵️♂️ Deduction

Mixed-use vehicle

🔍 Missed Evidence:

No distinction between personal and business use

⚠️ Red Flag:

100% business claim on a shared vehicle

💡 Defense Strategy:

Separate business and personal trips using consistent tracking

A business owner has ongoing vehicle costs throughout the year.

Fuel here. Repairs there. Insurance paid automatically.

Some are remembered. Others are not.

At year end, the total is incomplete.

Another business owner pays for everything through the business and lets the records build naturally.

Nothing complicated.

Just consistent.

Now the full cost is visible.

🕵️♂️ Deduction

Ongoing vehicle expenses

🔍 Missed Evidence:

Expenses not recorded consistently

⚠️ Red Flag:

Vehicle use suggests higher costs than reported

💡 Defense Strategy:

Record expenses as they occur and keep them tied to the business

A business owner purchases a vehicle and uses it regularly for work.

But the purchase is treated casually.

No clear connection to the business is established.

Another business owner uses the vehicle in a way that is obviously tied to operations.

Client visits. Job sites. Daily activity.

Now the role of the vehicle is clear.

🕵️♂️ Deduction

Vehicle tied to business activity

🔍 Missed Evidence:

No clear link between vehicle use and business function

⚠️ Red Flag:

Vehicle appears primarily personal

💡 Defense Strategy:

Ensure business use is consistent and easy to recognize through normal activity

As the business grows, so does the driving.

More clients.

More locations.

More movement.

The vehicle becomes part of how the business operates.

And when that use is captured properly, the cost follows naturally and reduces the income being taxed.

Where this breaks down is not complexity.

It’s inconsistency.

No tracking.

No separation.

No record of how the vehicle is actually used.

But when handled the way most real businesses operate…

You drive.

The app tracks.

The record builds.

And the deduction reflects what already happened.

That is how this category is meant to work.

Not as extra work.

But as something that runs quietly in the background while the business moves forward.

🕵️♂️ #7: S-Corp Compensation

How You Pay Yourself Changes What You Keep

Most business owners look at how much they made.

Fewer look at how they paid themselves.

That second part is where the shift happens.

A business owner earns $120,000.

They operate as a sole proprietor.

All $120,000 is treated the same.

It is all subject to income tax and self-employment tax.

Nothing is separated.

Now take the same $120,000.

The business elects S-Corp status.

Instead of everything being treated the same, it is split.

Salary: $60,000

Distributions: $60,000

The total income is still $120,000.

That doesn’t change.

But how it is treated does.

The $60,000 salary is subject to payroll taxes.

The $60,000 distribution is not.

That’s where the difference shows up.

In simple terms, roughly 15% self-employment tax applies to the salary portion.

On $60,000, that’s about $9,000.

The remaining $60,000 avoids that layer.

Same income.

Different structure.

Different outcome.

🕵️♂️ Deduction

S-Corp compensation split

🔍 Missed Evidence:

No clear basis for how salary was determined

⚠️ Red Flag:

Salary set unrealistically low compared to total income

💡 Defense Strategy:

Set salary based on what someone would reasonably be paid to do that role

Now look at the same situation without the structure.

A business owner earns $120,000 and does nothing differently.

All of it is treated as self-employment income.

That same 15% applies across the board.

Now the self-employment tax is closer to $18,000.

Same $120,000.

No split.

No adjustment.

The extra cost is simply absorbed.

🕵️♂️ Deduction

Unstructured owner compensation

🔍 Missed Evidence:

No separation between earned income and ownership income

⚠️ Red Flag:

All income treated the same regardless of role

💡 Defense Strategy:

Introduce structure that reflects both the work performed and ownership of the business

Now take it one step further.

A business owner sets salary too low.

Let’s say $20,000 salary and $100,000 distribution.

On paper, the tax looks minimized.

In reality, it creates imbalance.

The salary no longer reflects the work being done.

That gap becomes hard to justify.

Another business owner sets salary at a level that matches the actual work.

Not inflated.

Not minimized.

Just reasonable.

Now the structure holds.

🕵️♂️ Deduction

Reasonable compensation

🔍 Missed Evidence:

No connection between duties performed and salary level

⚠️ Red Flag:

Large gap between salary and total income

💡 Defense Strategy:

Keep salary aligned with real responsibilities and industry norms

Now add one more layer that most overlook.

A business owner pays for business expenses personally.

Mileage.

Home office use.

Supplies.

Nothing is reimbursed.

Those costs are either missed or handled inconsistently.

Another business owner runs those same expenses through the business using a simple reimbursement approach.

Let’s say $10,000 of legitimate business expenses were paid personally during the year.

The business reimburses that $10,000.

That reimbursement is not treated as income to the owner.

The business deducts it.

Now the taxable income drops from $120,000 to $110,000.

No change in actual cash position.

Just proper recognition of expenses.

🕵️♂️ Deduction

Reimbursed business expenses

🔍 Missed Evidence:

Expenses paid personally with no record or reimbursement

⚠️ Red Flag:

Business activity exists but expenses are missing from records

💡 Defense Strategy:

Track and reimburse legitimate business expenses through the business

There’s also a practical side to this.

Without structure, money moves randomly.

Withdrawals happen when needed.

Nothing is clearly defined.

With structure, payroll runs consistently.

Distributions are separate.

Reimbursements are clean.

Now the flow of money reflects what is actually happening.

🕵️♂️ Deduction

Structured payroll, distributions, and reimbursements

🔍 Missed Evidence:

No distinction between salary, distributions, and expense recovery

⚠️ Red Flag:

All money flowing without clear classification

💡 Defense Strategy:

Separate salary, distributions, and reimbursements so each serves its purpose

This is not about reducing income.

The income stays the same.

It’s about recognizing that part of what you earn is for the work you do, part of it is because you own the business, and part of it is simply getting your own money back.

When those are separated properly, the result changes.

Not through tricks.

Through structure.

That is how this category is meant to work.

Not by chasing deductions.

But by deciding how income flows in the first place.

🕵️♂️ #8: Home Office

When Your Home Isn’t Just Where You Live… It’s Where You Build

Most people think of a home office as a desk in a spare room.

That’s not what this is.

This is about when your home actually becomes part of your business.

Not technically.

Not on paper.

But in real life.

A consultant works from a dedicated room.

A coach runs sessions from home.

An online business operates entirely from a residential setup.

That’s common.

But sometimes it goes much further.

I had a tri-level home.

And the basement alone was the same size as the main floor.

That basement wasn’t storage.

That was my operation.

I was printing my own books down there using large color copiers.

That wasn’t a hobby setup. That was production.

Along with that, I had my business offices set up in the same space.

That entire lower level was being used to run the business.

And upstairs?

That wasn’t just home either.

I was meeting students and clients on the main floor.

So now the business wasn’t just in one room.

It was moving through the house.

When I actually looked at it honestly and measured it properly, about 50% of the total square footage of the home was being used for business.

Not stretched.

Not pushed.

Just real.

And once that was clear, everything connected to that space followed.

Mortgage.

Utilities.

Internet.

Maintenance.

Half of those costs were tied directly to the business.

That wasn’t a trick.

That was just recognizing how the business was actually operating.

And let me tell you, that was a rather sizable deduction!

🕵️♂️ Deduction

Home used as a real operating base

🔍 Missed Evidence:

No clear explanation of how the space is actually used

⚠️ Red Flag:

Large percentage claimed with no visible business activity

💡 Defense Strategy:

Let the usage speak and support it with reasonable measurement

Most people go the other direction.

They use their home for business every day and claim almost nothing.

They sit at the same desk.

Use the same internet.

Run their business from the same space.

But never connect it.

So the cost stays personal.

🕵️♂️ Deduction

Underused home office

🔍 Missed Evidence:

No measurement or tracking of space used

⚠️ Red Flag:

Business clearly operating from home with no corresponding deduction

💡 Defense Strategy:

Identify the space, measure it, and apply it consistently

Then there’s the opposite.

Someone tries to claim the entire home with no real basis.

That doesn’t hold.

This only works when it reflects reality.

🕵️♂️ Deduction

Overstated home use

🔍 Missed Evidence:

No clear boundary between personal and business space

⚠️ Red Flag:

Entire home claimed without justification

💡 Defense Strategy:

Stay grounded in actual usage and apply a reasonable percentage

The strength of this deduction isn’t in squeezing numbers.

It’s in telling the truth clearly.

If your business lives in your home, then part of your home belongs to your business.

And when that’s handled properly, the costs follow naturally.

That is how this category is meant to work.

Not as a technical calculation.

But as a reflection of how your business actually lives and operates.

🕵️♂️ #9: Health Insurance

One of the Few Personal Costs That Becomes a Direct Business Advantage

Most expenses in a business are obvious.

Health insurance isn’t.

It feels personal.

It feels separate.

But for a business owner, it sits right at the intersection of both worlds.

You need it personally.

But when structured properly, it becomes a direct reduction of your taxable income.

A business owner pays $12,000 a year in health insurance.

If nothing is done intentionally, that cost is just absorbed.

Paid.

Forgotten.

Another business owner pays the same $12,000.

But now it’s connected to the business.

That $12,000 reduces taxable income.

Same expense.

Different outcome.

🕵️♂️ Deduction

Self-employed health insurance

🔍 Missed Evidence:

Premiums paid but not connected to business income

⚠️ Red Flag:

Insurance exists but no deduction is taken

💡 Defense Strategy:

Ensure premiums are tied to the business and properly reported

There’s a simple reality here.

If you’re self-employed and paying for your own health insurance, that cost is not just personal.

It’s part of the cost of operating your life while running your business.

And the system recognizes that.

But only if it’s claimed.

Another situation shows up with structure.

A business owner operates through an S-Corp.

The policy is in their personal name.

Premiums are paid personally.

Nothing is done beyond that.

The deduction is either missed or not handled correctly.

Another business owner runs those same premiums through the business properly.

Now the cost is clearly tied to the business, and the deduction flows through correctly.

🕵️♂️ Deduction

Health insurance through an S-Corp structure

🔍 Missed Evidence:

Premiums paid personally with no connection to business reporting

⚠️ Red Flag:

Insurance expense exists but is not reflected properly in income structure

💡 Defense Strategy:

Run premiums through the business in a way that aligns with how compensation is reported

There’s also a family component that many overlook.

A business owner pays for their own coverage, their spouse, and their dependents.

The total adds up.

If handled properly, that full amount can reduce taxable income.

If ignored, it becomes a large personal expense with no benefit on the tax side.

🕵️♂️ Deduction

Family health insurance coverage

🔍 Missed Evidence:

Only partial premiums considered or none at all

⚠️ Red Flag:

High insurance cost with little or no deduction

💡 Defense Strategy:

Include all eligible coverage tied to the business owner and family

Another pattern shows up quietly.

A business owner has access to coverage through a spouse’s employer but chooses their own plan.

That changes eligibility.

This is one of the few areas where availability matters, not just what you choose.

🕵️♂️ Deduction

Eligibility limitations

🔍 Missed Evidence:

No consideration of alternative coverage availability

⚠️ Red Flag:

Deduction taken when other employer coverage was available

💡 Defense Strategy:

Be aware of eligibility rules and how access to other plans affects the deduction

There’s a practical side to this.

Health insurance is one of the larger recurring costs most business owners carry.

Month after month.

Year after year.

Handled passively, it’s just another bill.

Handled properly, it becomes one of the cleanest ways to reduce taxable income without changing anything about how you live.

You’re already paying it.

The only question is whether it’s working for you.

Where this breaks down is simple.

Not claiming it.

Not structuring it.

Not connecting it to the business.

At that point, the benefit is lost.

But when handled the way real businesses operate…

The expense is real.

The coverage is necessary.

And the deduction follows naturally.

That is how this category is meant to work.

Not as a technical loophole.

But as a recognition that protecting your health is part of running your business.

🕵️♂️ #10: Rent

When the Space You Pay For Clearly Belongs to Your Business

Rent is one of the cleanest deductions there is.

If you are paying for space to run your business, that cost is part of doing business.

A therapist rents an office.

A trainer rents studio space.

A contractor rents a warehouse.

A consultant leases a small office outside the home.

That payment is not optional.

It is the cost of having a place to operate.

And when that space is genuinely used for business, the deduction follows naturally.

A business owner pays $2,000 a month in rent.

That is $24,000 a year.

If that space is being used to run the business, that full amount reduces taxable income.

Simple.

Direct.

Clean.

🕵️♂️ Deduction

Business rent

🔍 Missed Evidence:

Lease or payments not clearly tied to the business

⚠️ Red Flag:

Rent exists but is not reflected in business records

💡 Defense Strategy:

Keep lease agreements and payments clearly connected to the business

Now here is where real life comes in.

You rent a warehouse.

You run your business there every day.

Equipment is stored there.

Work happens there.

Operations are based there.

That is clearly a business space.

Now something else happens.

You have a few friends over after hours.

Or you allow a family member to use the space occasionally.

Life happens.

That does not automatically undo the deduction.

The key question is not whether anything personal ever happens in the space.

The question is whether the space clearly exists for business.

🕵️♂️ Deduction

Primarily business use of rented space

🔍 Missed Evidence:

No clear connection between the space and daily business activity

⚠️ Red Flag:

Space appears to serve multiple unrelated purposes

💡 Defense Strategy:

Ensure the business use is consistent, obvious, and central to why the space exists

Now let’s draw a clear boundary.

Occasional use is one thing.

Recurring, structured non-business use is another.

If a warehouse is used every day for business, and once in a while something personal happens, that is incidental.

But if that same space is used on a regular, ongoing basis for something else, every week, organized, predictable, and unrelated to the business, then the space starts to look like it serves two purposes.

That is where judgment comes in.

🕵️♂️ Deduction

Dual-use risk

🔍 Missed Evidence:

No distinction between primary business use and recurring alternate use

⚠️ Red Flag:

Regular non-business activity that looks like a second function of the space

💡 Defense Strategy:

Keep the space clearly business-first and avoid patterns that redefine its purpose

This is not about perfection.

No one is expecting a business space to be used with zero overlap of real life.

But it must be clear what the space is for.

If someone looked at it, the answer should be obvious.

This is where the business operates.

Everything else is secondary.

There is also a practical side to this.

As your business grows, space becomes more important.

More inventory.

More equipment.

More activity.

Rent becomes a steady, predictable cost that directly reduces taxable income.

Handled properly, it is one of the most straightforward deductions available.

Where this breaks down is simple.

Payments not tracked.

Space not clearly tied to business activity.

Usage drifting into something that no longer looks primarily business.

At that point, even a valid expense becomes harder to defend.

But when handled the way real businesses actually operate…

You rent the space because you need it.

You use it to run the business.

You record the cost properly.

And the deduction follows.

That is how this category is meant to work.

Not by stretching definitions.

But by making sure the space you pay for clearly belongs to your business.

🕵️♂️ At Tax Ready Ledger Co., we don’t just track your numbers… we structure them so they make sense, hold up, and work in your favor. Learn more at taxreadylc.com.

🕵️♂️ #11: Retirement Contributions

Pay Yourself Later… and Pay Less Now

Most people with regular jobs don’t think much about retirement. It’s built into the system. Money gets taken off the top, plans are already in place, and contributions happen whether they pay attention or not.

A business owner doesn’t have that luxury. There is no automatic system unless you create one. Which means this becomes a decision… and that’s where things quietly go off track.

The business starts doing well. Income increases. There’s more breathing room. And naturally, the focus shifts to enjoying it a little more. Nothing wrong with that. In fact, it’s part of why you built the business in the first place.

But time has a way of moving faster than expected. One year turns into five. Five turns into ten. And suddenly your strongest earning years are not in front of you… they’re behind you.

Now you’re playing catch-up.

And that’s a much harder game. Not just financially, but from a tax standpoint too. Because every year you didn’t contribute, you didn’t just miss savings… you missed clean, legitimate deductions that could have reduced your taxable income all along.

A business owner earns $160,000 and keeps all of it available. That full amount is exposed to income tax.

Another business owner earns the same $160,000 but contributes $30,000 into a retirement plan. Now only $130,000 is exposed to tax.

Same income. Different outcome.

🕵️♂️ Deduction

Retirement contribution reducing taxable income

🔍 Missed Evidence:

No contributions made despite strong income

⚠️ Red Flag:

High earnings with no long-term structure in place

💡 Defense Strategy:

Treat contributions as part of the business system, not something optional

What makes this different from most deductions is simple. You’re not spending the money. You’re repositioning it. It still belongs to you. It’s just working somewhere else, while reducing what gets taxed today.

Over time, the gap becomes obvious. One business owner pays full tax year after year and hopes to save what’s left. Another builds contributions into their operating rhythm. Money moves before it becomes fully taxable, and the benefit shows up immediately.

🕵️♂️ Deduction

Consistent retirement funding

🔍 Missed Evidence:

No pattern or discipline in contributions

⚠️ Red Flag:

Income increases but savings and deductions do not

💡 Defense Strategy:

Make contributions part of your normal flow, not a year-end decision

There’s also a scale component that most people underestimate. Small, occasional contributions help, but they don’t move the needle much. Plans like SEP-IRA or Solo 401(k) allow significantly higher contributions when income supports it. When those are used properly, the shift becomes meaningful.

🕵️♂️ Deduction

Maximized contribution limits

🔍 Missed Evidence:

Only minimal contributions despite higher eligibility

⚠️ Red Flag:

Underutilized capacity relative to income level

💡 Defense Strategy:

Understand what’s available and use it when the business allows it

Timing plays a role as well. Some contributions can be made after year end and still apply to the previous year. Miss that window and the opportunity is gone. Catch it, and you still control where the deduction lands.

🕵️♂️ Deduction

Timing of contributions

🔍 Missed Evidence:

Missed deadlines or reactive decisions

⚠️ Red Flag:

Inconsistent or last-minute contributions

💡 Defense Strategy:

Stay aware of deadlines and act intentionally

There’s a line that sums this up better than anything.

“If I knew I was going to live this long, I would have taken better care of myself.”

That wasn’t said about taxes… but it might as well have been.

Because the earlier you build this into your system, the easier everything becomes. And the longer you wait, the harder it is to make up the ground you lost.

Where this breaks down is simple. No structure. No consistency. Too much focus on today, not enough on what comes next.

But when handled the way real business owners eventually learn to operate, income is earned, a portion is set aside, taxable income drops, and that money continues working quietly in the background.

That is how this category is meant to work.

Not as something you get around to…

…but something you decide early, while it still matters.

🕵️♂️ #12: Education

When Learning Strengthens the Business… and Sometimes Expands It

Education is one of those deductions that sounds simple until you look a little deeper.

A business owner takes a course, buys a program, joins a coaching group, or attends a workshop. The instinct is to write it off. Sometimes that works. Sometimes it doesn’t.

The foundation is straightforward.

The education must improve or support the business you are already operating.

Not prepare you for something unrelated.

That’s the anchor.

A consultant sharpens their expertise. A coach improves how they attract and serve clients. A contractor learns better ways to deliver their work. That strengthens the existing business, and the cost is clearly tied to income.

Now it holds.

A business owner earning $240,000 invests $12,000 into a program that improves lead generation, delivery systems, or client retention. That $12,000 reduces taxable income because it directly supports how the business operates and grows.

Another business owner spends the same $12,000 preparing for a completely different career with no connection to the current business.

Same money. Different intent. Different result.

🕵️♂️ Deduction

Education tied to current business

🔍 Missed Evidence:

No clear link between the training and the business activity

⚠️ Red Flag:

Course appears to prepare for a different profession

💡 Defense Strategy:

Make sure the education clearly improves or supports the current business

Now here’s where most people stop.

But this is where Tax Intelligence begins.

A business owner runs an online company with a growing team. Revenue is strong, but there’s a recurring issue. Staff productivity dips. People leave early. Schedules get disrupted because of childcare responsibilities.

Instead of accepting that as a cost of doing business, the owner looks at it differently.

What if that problem could be solved inside the business?

Not by launching a daycare.

Not by changing careers.

But by improving how the business operates.

Now the owner invests in training around childcare systems and small-scale implementation. The goal isn’t to become a childcare provider to the public. The goal is to understand how to create a controlled, internal solution that supports employees and stabilizes operations.

The connection is clear.

The purpose is practical.

The training strengthens the business.

🕵️♂️ Deduction

Education tied to operational expansion within the same business

🔍 Missed Evidence:

No documented connection between training and business need

⚠️ Red Flag:

Education appears to lead to a separate, unrelated business

💡 Defense Strategy:

Tie the learning directly to improving operations, employee performance, or retention

Now compare that to a different path.

A business owner takes the same childcare training and then opens a separate daycare business for the public.

Now it’s a new trade.

That’s where the deduction breaks.

The difference isn’t the course.

It’s the role it plays.

There’s also a level most people overlook.

Education doesn’t have to be formal.

It can be books, online programs, coaching, workshops, or subscriptions tied to learning. If it improves how you run your business, it can qualify.

A business owner consistently invests in learning that sharpens their edge. Better systems, better communication, better execution. That cost becomes part of how they operate.

Another business owner avoids investing in learning altogether. The business plateaus. No expense. No deduction. No growth.

🕵️♂️ Deduction

Ongoing business education

🔍 Missed Evidence:

No tracking of learning-related expenses

⚠️ Red Flag:

Business growth claimed without investment in development

💡 Defense Strategy:

Capture all learning that directly improves business performance

Timing matters as well.

Education taken while the business is active is much easier to support than education taken before anything exists. Once the business is operating, the connection becomes clear.

🕵️♂️ Deduction

Timing of education

🔍 Missed Evidence:

Training taken before business activity begins

⚠️ Red Flag:

Costs appear preparatory rather than operational

💡 Defense Strategy:

Tie education to an active, ongoing business

The strength of this deduction comes down to clarity.

Is this making the business better?

Or is this preparing you to do something else?

That’s the question.

Where this breaks down is predictable. Trying to force unrelated learning into the business, losing the connection between training and income, or relying on intention instead of reality.

But when handled the way real business owners operate, learning becomes part of the system. The business improves. The connection is obvious. And the deduction follows.

That is how this category is meant to work.

Not by stretching definitions…

…but by structuring growth so it clearly belongs to the business you already have.

🕵️♂️ #13: Software

From Small Monthly Tools… to Systems That Run the Business

Software is one of the most overlooked categories because it feels ordinary.

A small monthly charge here.

A subscription there.

A tool you barely think about once it’s set up.

But in today’s business world, software isn’t optional.

It’s infrastructure.

A designer uses Canva.

A coach uses Zoom and a CRM.

A service business uses scheduling, invoicing, and communication tools.

An online company runs entire operations through platforms and automation systems.

Some of these cost a few hundred dollars a year.

Others run into the thousands, even tens of thousands when the system becomes central to the business.

All of it matters.

A business owner spends $300 a year on basic tools like Canva or email platforms. It’s small, easy to overlook, and often not tracked carefully.

Another business owner runs $15,000 to $30,000 a year through software. CRM systems, automation platforms, payment integrations, analytics, hosting, communication tools. These are not extras. These are what keep the business moving.

Same category. Different scale.

🕵️♂️ Deduction

Core business software

🔍 Missed Evidence:

Subscriptions scattered across accounts and not fully captured

⚠️ Red Flag:

Business clearly relies on software but expenses are minimal or incomplete

💡 Defense Strategy:

Track all subscriptions in one place so the full cost is visible

Now look at how this gets missed in real life.

A business owner signs up for multiple tools over time. $29 here. $79 there. $199 somewhere else. Individually they feel small, so they don’t get attention.

But over a year, those same charges can quietly add up to several thousand dollars.

Another business owner captures everything. Every subscription, every renewal, every platform. Nothing is left to memory. Now the total reflects reality.

🕵️♂️ Deduction

Accumulated software expenses

🔍 Missed Evidence:

Small recurring charges not tracked consistently

⚠️ Red Flag:

Fragmented expenses with no central record

💡 Defense Strategy:

Group and track all software so the total reflects reality

There’s another layer most people overlook.

Some software only becomes useful when it is properly implemented.

A business owner invests in a system but never learns how to use it effectively. The cost is there, but the benefit is limited.

Another business owner invests not just in the software, but in the training required to actually use it. Now the system supports the business the way it was intended.

🕵️♂️ Deduction

Software-related training

🔍 Missed Evidence:

Training costs not connected to the systems they support

⚠️ Red Flag:

Large software expense with little operational impact

💡 Defense Strategy:

Tie training directly to the systems being used in the business

As the business grows, something shifts.

At the beginning, software supports the business.

Over time, software begins to run the business.

Automation replaces manual work. Systems replace guesswork. Processes become consistent.

At that point, software is no longer a convenience. It becomes part of the operating model.

🕵️♂️ Deduction

Operational software systems

🔍 Missed Evidence:

No distinction between casual tools and core systems

⚠️ Red Flag:

Business depends on systems but records don’t reflect the cost

💡 Defense Strategy:

Recognize and track software as a core operating expense

The strength of this category isn’t complexity.

It’s consistency.

Most software expenses are fully deductible when they are used in the business.

The problem isn’t qualification.

It’s capture.

Where this breaks down is predictable. Subscriptions get forgotten, charges are spread across different cards, and there is no system to track recurring costs.

At that point, money is being spent, but not fully recognized.

But when handled the way real businesses operate, every tool is accounted for, every system is tracked, and every cost is visible.

And the deduction reflects what the business is actually running on.

That is how this category is meant to work.

Not as a handful of small charges…

…but as the backbone of how modern businesses operate.

🕵️♂️ #14: Professional Fees

When Paying for Expertise Becomes a Direct Reduction of Taxable Income

Professional fees are one of the cleanest deductions available.

If you pay someone for services that support your business, that cost reduces your taxable income.

That’s the focus.

Not why you hired them.

Not when you hired them.

Just whether the service is tied to the business.

Accountants.

Bookkeepers.

Lawyers.

Consultants.

Specialists brought in to solve specific problems.

If their work relates to your business operations, compliance, structure, or problem-solving, the cost is deductible.

A business owner earning $180,000 pays $6,000 to an accountant and bookkeeper. That $6,000 reduces taxable income directly because it supports the business.

Simple.

🕵️♂️ Deduction

Professional fees tied to business activity

🔍 Missed Evidence:

No clear record of what service was provided

⚠️ Red Flag:

Fees paid with no identifiable connection to the business

💡 Defense Strategy:

Ensure invoices or descriptions clearly reflect the business purpose of the service

Now here’s where tax intelligence shows up.

A cost that looks personal or unrelated at first glance can become fully deductible when its connection to the business is clear.

A business owner hires a tree removal service.

On the surface, that looks like a personal expense.

But the facts tell a different story.

The tree is obstructing the entrance to the business.

It affects access for clients or deliveries.

It blocks natural light, making the workspace less functional.

Now the purpose is not cosmetic.

It’s operational.

The cost is tied directly to how the business functions.

That changes everything.

🕵️♂️ Deduction

Service reclassified through business purpose

🔍 Missed Evidence:

No explanation of how the expense impacts business operations

⚠️ Red Flag:

Expense appears personal with no documented business connection

💡 Defense Strategy:

Clearly tie the service to access, safety, or functionality of the business

Same service.

Different context.

Different result.

Another business owner removes a tree purely for personal preference at their residence with no connection to business use.

That cost stays personal.

The difference is not the expense.

It’s the purpose.

There’s also a practical detail that gets missed.

A business owner pays for services from a personal account and never records them properly. Some expenses are remembered, others are not.

Another business owner tracks and records every service tied to the business.

Now the full deduction is captured.

🕵️♂️ Deduction

Captured service-based expenses

🔍 Missed Evidence:

Payments made but not recorded in the business

⚠️ Red Flag:

Business activity suggests expenses that are not reflected

💡 Defense Strategy:

Record all service-related costs that support the business

The strength of this category is clarity.

If the service supports the business, it is deductible.

If it doesn’t, it isn’t.

There’s no need to stretch it.

But there is every reason to recognize when a cost that seems personal is actually tied to how the business operates.

That is where most people miss it.

And that is where the advantage shows up.

That is how this category is meant to work.

Not by guessing…

…but by identifying what the expense actually does for the business.

🕵️♂️ #15: Meals (Structured)

Turning a 50% … into a 100% Deduction

Meals are one of the most misunderstood deductions in business.

Most people stop at this:

Client lunch → 50%

And that’s where they stay.

But that’s not the full picture.

Because the treatment of a meal is not about the food.

It’s about the purpose and structure behind it.

That’s what determines whether it stays at 50%… or moves to 100%.

A business owner earning $210,000 spends $6,000 a year on client lunches. Those meals are directly tied to business discussions, so they qualify.

But they are considered entertainment-related meals.

So only 50% is deductible.

$3,000 reduces taxable income.

The other $3,000 does nothing.

Same meals.

Now watch what happens when structure changes.

🕵️♂️ Deduction

Business meals at 50%

🔍 Missed Evidence:

No documentation of business purpose or attendees

⚠️ Red Flag:

Meals with no clear business discussion

💡 Defense Strategy:

Record who attended and the business purpose of the meeting

Now let’s move into Tax Intelligence.

A business owner hosts a paid workshop.

Food is provided to attendees as part of the event.

Now the meal is no longer a side activity.

It becomes part of delivering the service.

That changes the category.

Now it’s 100% deductible.

🕵️♂️ Deduction

Meals as part of a paid event or service

🔍 Missed Evidence:

No connection between the food and the business event

⚠️ Red Flag:

Food appears incidental rather than part of the service

💡 Defense Strategy:

Tie the meal directly to the event offering or delivery

Another business owner hosts an open house or promotional event.

Food is provided to attract potential clients.

Now the meal becomes marketing.

Again, 100% deductible.

🕵️♂️ Deduction

Meals as marketing or promotion

🔍 Missed Evidence:

No documentation that the event was business-related

⚠️ Red Flag:

Food provided with no clear promotional purpose

💡 Defense Strategy:

Document the event and its purpose as client acquisition or promotion

Now let’s go deeper.

A business owner purchases $100 restaurant certificates and distributes them as part of a client promotion.

This is not a meal anymore.

It’s a marketing expense.

100% deductible.

Later, those certificates are used during client meetings.

The key is not how they’re redeemed.

The key is how they were structured and classified when issued.

🕵️♂️ Deduction

Meal reclassified as marketing through promotional structure

🔍 Missed Evidence:

No record showing certificates were used as a promotion

⚠️ Red Flag:

Certificates treated inconsistently between marketing and meals

💡 Defense Strategy:

Document the intent as a promotional campaign when issued

Now another scenario.

Employees are working overtime.

Food is brought in so work can continue.

This is not entertainment.

This is supporting operations.

That shifts the treatment.

Now it becomes 100% deductible.

🕵️♂️ Deduction

Meals for employee convenience

🔍 Missed Evidence:

No indication that meals were tied to work conditions

⚠️ Red Flag:

Food provided without connection to business necessity

💡 Defense Strategy:

Tie meals to overtime, productivity, or workplace necessity

Same food.

Different structure.

Different outcome.

That’s the pattern.

Meals that are social or discussion-based tend to stay at 50%.

Meals that are integrated into operations, marketing, or service delivery move to 100%.

That’s the shift.

Where this breaks down is simple.

No documentation.

No defined purpose.

Treating everything the same.

At that point, everything defaults to 50%… or worse, gets disallowed.

But when handled properly, meals become one of the most flexible categories available.

Not because the rules are loose.

But because the structure can change the classification.

And when the classification changes…

The deduction changes with it.

That is how this category is meant to work.

Not by accepting the default…

…but by understanding what actually determines the percentage.

🕵️♂️ At Tax Ready Ledger Co., we don’t just track your numbers… we structure them so they make sense, hold up, and work in your favor. Learn more at taxreadylc.com.

🕵️♂️ #16: Merchant Fees

The Hidden Deduction Inside Every Sale

Merchant fees are one of the most consistent deductions in a service-based business.

And one of the most misunderstood.

Because most business owners think like this:

“I only received what hit my bank account… so that must be my income.”

That sounds logical.

But it’s wrong.

Income is the gross amount charged to the customer.

The merchant takes their cut.

That cut is not reducing your income.

It is a business expense.

And that’s where the deduction lives.

A client pays you $300 using a credit card.

The processor connected to Visa, Mastercard, American Express, or Discover deposits $291.30 into your bank.

It feels like you made $291.30.

But you didn’t.